Related Articles

In recent days, the establishment media have begun the push to shape the post-pandemic narrative. The massive influx of state funding to prevent the economy from collapsing entirely will have to be repaid one way or another; and the SW1 crowd are determined to pass the bill on to someone else. That is, you and me. As Dharshini David at the BBC puts it:

“This year’s deficit could be the equivalent of the biggest slice of our income since the Second World War – and that hole needs plugging.

“For the moment, the government has increased its borrowing on financial markets, through bonds, effectively IOUs – but there is a limit to how much it can do so.

“Ultimately, economists say taxes will have to rise, or spending cut – the emergency raft will have a price tag which we can’t escape.”

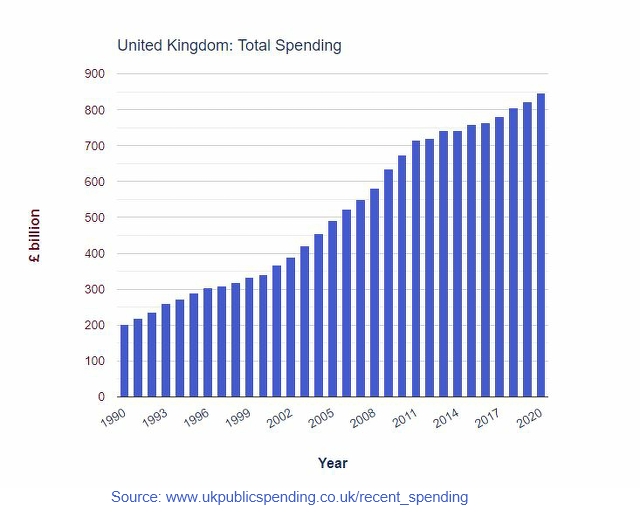

Tax increases are favoured by the establishment because they fall disproportionately on the shoulders of ordinary people – who don’t have access to offshore tax havens or to expensive specialist tax avoidance accountants. Public spending cuts inflict misery on those at the very bottom of the income ladder – who only pay (regressive) indirect taxes such as VAT – but are so expensive to administer that they have little impact on overall state spending; which continues to increase:

Most often, “spending cuts” are no more than an accounting trick designed to move state spending off the books via various forms of Public Private Partnerships – which were developed as a means of getting around European Union state aid rules (which prevent member governments from directly subsidising industries, businesses and services). The public services remain the same, and it is only when things go wrong that we discover that Carillion is providing school diners or that Richard Branson is responsible for cleaning our hospitals. It goes without saying that the services are worse when delivered by cost-cutting corporate welfare recipients than they had been when delivered in-house.

This said it would be wrong to think that we are not going to have to pay a price for the emergency state spending to fight the pandemic. As the first sentence in any economics text book ought to say: you can print currency but you can’t print wealth.

This brings us to the two – entirely wrong – narratives that we are about to be offered. The establishment will try to convince us that state spending is always bad because it “crowds out” more efficient private activity (funny how those who are the loudest in advocating free markets are the first in line for a state handout in a crisis). The job of government – they will tell us – is to balance the books (but not by raising their taxes or by cutting their corporate welfare handouts). It is for the entrepreneurial private sector to generate the economic growth which, in turn, will generate the additional tax revenue to repay the debt.

The left, meanwhile, will offer us an equally wrong narrative – that the role of the state is to counterbalance the cycles of boom and bust of the markets. It is precisely at the point when private markets have slumped that the state needs to step in as the purchaser/investor of last resort, to maintain the economy and to nurture the green shoots of recovery.

Politically, no doubt, most of the population will divide into the usual blue and red teams; the blue (Tory) team cheering for cuts while the red (Labour) team calls for more spending and more borrowing. Only a small minority will take the step back – and face the inevitable slurs – to look at the broader picture.

The reason both narratives are wrong stems from their respective misunderstanding of what value is and how value is added. Those on the political right tend to dismiss the concept of intrinsic value entirely – arguing that “exchange value” is all there is. The value of a good or service is solely a function of market supply and demand – it is worth whatever people are prepared to pay for it. Those on the left tend to accept some version of Adam Smith’s “labour theory of value.” According to Smith (The Wealth of Nations, Book 1, Chapter 6):

“If among a nation of hunters, for example, it usually costs twice the labour to kill a beaver which it does to kill a deer, one beaver should naturally exchange for, or be worth two deer. It is natural that what is usually the produce of two days’ or two hours’ labour, should be worth double of what is usually the produce of one day’s or one hour’s labour.”

Marx refined this by separating use value from exchange value and by adding the idea of “socially necessary labour.” Thus the value of something is different to its price, and is determined by the average labour time across the economy to produce it rather than the time a (possibly incompetent) worker might happen to take.

Marx developed this further to introduce us to the first version of the capitalist money trick. Money is not valuable in and of itself, but is merely a claim on value in the form of the goods, services, work and land that it might buy. In a capitalist economy, investors seek to use the process of production to end up with more money than they invested in the first place:

The commodities or widgets – “C” – which a capitalist firm produces are only of secondary concern. The point is to invest less money in the machinery (capital) resources and labour required to produce the commodities than the commodities can be sold for at the end of the process. It follows that one or other of the inputs to the productive process must be paid less than it is worth. Marx was both clear – and in error – about which (Wage-Labour and Capital/Value, Price and Profit.):

“The values of commodities are directly as the times of labour employed in their production, and are inversely as the productive powers of the labour employed… Take the example of our spinner. We have seen that, to daily reproduce his labouring power, he must daily reproduce a value of three shillings, which he will do by working six hours daily. But this does not disable him from working ten or twelve or more hours a day. But by paying the daily or weekly value of the spinner’s labouring power the capitalist has acquired the right of using that labouring power during the whole day or week.”

In short, by paying workers for their time rather than for the value they add to production, capitalists reap the “surplus value” – the unpaid labour of the working class. This, though, sets up the fundamental flaw in the capitalist system. Since workers are paid for their time rather than the value they add, there is never sufficient purchasing power in the economy to buy back all of the goods and services that are produced. Sooner or later, businesses will begin to fail because they cannot sell enough of their goods and services to remain profitable. They will find various ways of cutting wages and increasing the workload, but this merely delays the day of reckoning because it removes even more purchasing power from the economy. Depression eventually sets in as business failures grow, workers are laid off and investors cannot make profits.

Although Amazon founder Nick Hanauer might baulk at being labelled a Marxist, the crisis – and solution – set out in his once banned 2012 TED talk is precisely the crisis set out by Marx. When it comes to value, however, it is mistaken. Although labour power is a source of value it is not the only or even a particularly powerful source of value. Marx appears to have glimpsed this in developing the Grundrisse – the blueprint for the ten volumes of Das Kapital that he intended writing (he only completed the first volume; Engels completed volumes two and three from Marx’s notes). There, he begins to acknowledge that the massive machinery of an industrialised economy might also be a source of value. Given that this would nullify his political conclusions, he rejected the idea; which was in error anyway.

It was neither labour nor the machines that were the source of value in an English economy that Marx saw industrialise during his lifetime. Rather, it was the mountain of solar energy in the form of fossilised plants which lay beneath the British Isles which was the true source of value. In a far less productive pre-industrial economy, the energy derived from human labour would, indeed, have been a proportionately bigger source of value. Although even then, the economy would have depended upon animal, wind and water power. Moreover, even the strongest of human workers would struggle to do a fraction of the work that fossil fuels provide in an industrial economy.

A barrel of conventional crude oil contains the equivalent of roughly 4.5 years of continuous human labour; or around 11 years at 35 hours per week, 48 weeks of the year. But the capitalist doesn’t pay for the value of the fuel, merely the cost of extracting it. For a mere £49 (at pre-pandemic prices) the capitalist purchases £330,000 worth of work (at the current UK median wage). It is the exploitation of fossil fuels rather than the exploitation of labour which generates the vast majority of the surplus value in an industrial economy.

The ongoing struggle between business owners and workers over the relative share of the surplus value provided by exploited energy is real enough. But they are not the life and death class struggle propagated by Marx and Engels. The contradiction at the heart of capitalist market relations is real enough too – if the working class lacks the purchasing power to buy back the goods and services produced, then someone is going to go bust. This, though, is where the far more exploitative money trick comes into play.

Industrial civilisation is punctuated with what Marx called “crises of over-production” – in reality, crises of under-consumption – during which businesses cannot sell enough of the goods and services that they create to remain profitable. When this happens, businesses reach for solutions that require the workforce to take a cut in pay and for suppliers to cut their costs in order to stay afloat. Unfortunately, these only serve to remove even more purchasing power from the economy so that eventually firms go bust and the workforce gets fired. And so yet more purchasing power disappears. Worse still, investors and banks tend to become risk averse in such times leading to a lack of investment capital and to higher interest rates. Theoretically in a truly free market, the result would be that the least efficient (i.e. the most wasteful of energy) businesses would fail while the most efficient would continue to attract investment capital so that, eventually, a new growth cycle would begin. But free markets are like unicorns, homeopathic cures and honest politicians – they only exist as delusions.

Debt has always provided the means of extending and pretending that all is well in an economy which is fundamentally flawed. And no debt is stronger than the government/central bank debt which is issued against the taxes levied on future generations. For the moment at least, states like the USA and the UK can run up massive debts without needing to raise interest rates. And so long as they can do this they can act, in effect, as the borrower and consumer of last resort. Debt, however, introduces an even deadlier money trick than the one identified by Marx.

In the real world, those with the power to affect public policy have always sought to avoid the consequences of market economies. One way in which this used to be achieved was by encouraging governments to print new currency. This could then be used to prop up businesses which could not otherwise survive in a competitive environment. The quid pro quo was often either government taking a stake in the business or even taking complete ownership. This practice was wrongly (the underlying cause was the end of exponential growth in global oil extraction) believed to lie at the heart of the inflationary collapse of the post-war consensus in the 1970s. In the neoliberal system which replaced it, governments effectively privatised the money supply; handing responsibility for creating currency to the banking sector.

Governments and central banks would continue to exercise theoretical control over the supply of currency through a combination of regulation and the issuance of central bank reserves – a special currency used solely within the banking sector; but against which, ordinary bank loans can be made. While commercial banks that are in receipt of central bank reserves are able to create new currency out of thin air when they make loans to businesses and households. The process is no more than an accounting exercise in which the loan is added as an asset on the bank’s ledger and a liability to the borrower. This set up more or less allows banks to create as much new currency as they choose. (But remember: you can print currency but you can’t print wealth).

This raises serious problems in an economy which inevitably passes through cycles of boom and bust. In a boom period there is a huge incentive for banks to increase their lending far beyond that which a sober analysis would recommend. When this happens, a banking collapse only requires that the rate of borrowing slows down – it does not need to cease. This has happened several times between the 1986 “big bang” financial deregulation and the 2008 crash. Each time, rather than allow the most profligate banks to collapse, central banks and governments have intervened to bail them out; each time resulting in exponentially greater harm and costs than the previous one. What began as an attempt to stabilise inflation with minor changes to the rate of interest has resulted in negative (in real terms) interest rates and multi-trillion dollar bond buying programmes designed to insulate the banking and finance class from the consequences of their actions. Meanwhile, of course, businesses, households and the non-tax-raising arms of state have been starved of operating cash for more than a decade; grinding the “real” economy to a halt.

The contradiction at the heart of this money trick is that the only “value” behind the central bank currency which has been used to purchase all of these bonds and to maintain artificially low interest rates is the state’s ability to tax the wealth of the future population sufficiently to repay the debt with interest. This, in turn, requires that we somehow learn how to have infinite growth on a finite planet.

In the immediate aftermath of the 2008 crash, few serious analysts would have believed that the global system would have survived more or less intact for more than a decade. Conventional oil extraction had peaked in 2005 – triggering the chain of events which brought the banks down three years later. What nobody could have foreseen was the way that central bank manipulation would force investors who were seeking higher yields to invest in a hydraulic fracturing industry which borrowed billions of dollars from investors to extract millions of dollars’ worth of oil from the source rock. As Nicole Foss once put it – if conventional oil was like drinking draught beer from a glass, fracking was the equivalent of sucking the spilled dregs from the carpet.

Nevertheless, the spurt of oil from the US shale plays – which flooded the market and crashed the price – was just enough to prevent the western economies from collapsing while two Asian economies – India and especially China – turned to the last of the planet’s coal reserves to generate the final spurt of growth to an industrial economy that has now passed its peak.

While many will eventually blame the SARS-CoV-2 pandemic and the actions taken to mitigate its impact for the collapse of the global economy, the warning signs had already been apparent in 2019. Consumer spending had slumped and most consumer-facing businesses were being engulfed by a retail apocalypse which had only spared essentials like food together with a handful of online outlets which used gig-economy labour to keep costs down. Meanwhile, parking lots around the planet have been steadily filling up with new cars which can neither be sold nor leased to businesses and consumers who are already loaded up with debt and see little prospect of income/profit growth anytime soon.

The majority of economist and politicians – entirely ignorant of the role of energy in the economy – will assume that one or other means of reflating the currency supply in the aftermath of the pandemic – either through some equivalent of a long-term war bond to hold the pandemic debt or via government currency printing and public spending – will be sufficient to restore the economy to some version of “normal” (by which they usually mean the abnormal period of growth between 1953 and 1973). In the absence of an energy-dense alternative to depleting supplies of economically extractable oil, however, the trend away from automation toward manual labour which began after 2008 is likely to accelerate.

As real terms wages decline in response to this process of simplification, it will eventually become apparent to all concerned that the debt we have been running up on the assumption that growth will last forever is, in fact, never going to be repaid. When that happens, there will likely be a huge crash in the value of any “asset” that exists as mere bits on a bank computer. Hard assets like land and precious metals may experience a big rise in prices as those who manage to sell financial assets before the crash seek somewhere safe to park their wealth. But even these may be of little value – in the short-term at least – in the event that the value of currency itself collapses.

It has always been in the gift of governments to mitigate the coming downturn. A period of managed de-growth is far more preferable than a sudden anarchic collapse. Unfortunately, this would involve the ruling elite to acknowledge that a large part of its supposed wealth is going to disappear in any case. But no ruling elite has ever accepted this proposition at a point at which it might – just – save itself from its own folly. Instead, most failed civilisations spent their final years in a vain struggle to restore their fortunes long after the material bases had disappeared. The current media push for even more austerity and even more spending cuts at a time when both households and businesses are curbing their spending suggests that our civilisation will be no different.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.