Related Articles

Those lucky enough to die of old age often fall into a very peaceful state – not dissimilar to the deep relaxation sought after by meditation practitioners – from which they simply slip away. Since 1958, though, one of the ways in which modern civilisation has sought to cheat death has been to install pacemakers into the chests of people who develop irregular heartbeats. That was great while these people were in middle age, and might otherwise have had a premature death. But as the baby boomers enter their twilight years, more and more people will find themselves experiencing a phenomenon described by Nina Adamowicz some years ago:

“Adamowicz, then 71, described how she would lose consciousness, often at night, and would hear the click of her pacemaker snapping into action when she came to. She said she was ‘lucky’, and ‘forever grateful’for her life, but that she was also prepared to die.

“’I feel that [there is] life, and death is other side of the same coin,’ she said. ‘I’d like to know what is there. It’s not about I want to die, I’m dying’.

“So she asked for the pacemaker to be turned off.”

She became the first British pacemaker recipient to successfully campaign to have the device switched off. But in a civilisation that all too often denies the inevitability of death, and which is defaulted to extend life irrespective of individual wishes, Adamowicz had to battle to allow nature to take its course:

“Adamowicz went into her local hospice with her family and lay chatting while her doctor turned the pacemaker off, a procedure that took 20 minutes. She soon said she felt different, family members say. She described her body as feeling heavy and she felt a little nauseous, but said she felt at peace. She slept through the night, returned home in the morning and died later that night.”

The current iteration of the global economy – created by the collective unconscious decisions of baby boomers like Adamowicz – faces a similar moral decision. The economy’s pacemaker is central bank currency printing. And every time the economy slumps into that deep state from which death would ordinarily follow, the automatic central bank response is to use another massive influx of currency stimulation to kick the system back into life.

The first cardiac arrest came in 1973 with the first oil shock; which spelled the moment that the economy had to cease growing exponentially because the energy source that fuelled that growth had itself ceased growing exponentially. Sure, there was (and still is) more oil beneath the ground and sea bed than we have extracted and burned to date. But as the cost and complexity of oil extraction has grown, so the growth in the amount of energy available to power the economy has slowed.

Financialisation – the massive deregulation begun by Thatcher and Reagan and extended by Clinton and Blair – acted as the pacemaker; inflating a debt-based boom based on the fiction that there would be sufficient wealth in the future to pay off the debt with interest. Planet Earth, though, does not work that way. To have what humans call wealth, you have to have resources and you have to have the means to extract, transport and utilise these resources in order to create the goods and services that are bought and sold in the global marketplace. But before you can do any of that, you have to have energy. And while the new currency being borrowed into existence in the financialised economy was a claim on energy, it was not energy itself.

When conventional oil growth ceased entirely in 2005, it set in (slow) motion the chain of events which resulted in the 2008 financial crash and the decade of stagnation which followed. In summary:

- Lower oil supply led to higher oil prices

- Higher oil prices translated into higher prices across the economy

- Central banks raised interest rates to combat inflation

- Businesses and households that had previously managed to service their debts were plunged into arrears

- Insolvencies led to debt defaults which unravelled the complex webs of securities and insurances put in place by the banking system in an attempt to protect itself from the consequences of its greed

- States chose to bail out insolvent banks with the hypothetical taxes of future businesses and households (they could have let the banks fail and then nationalise their assets); thereby sucking the life out of the “real” economy.

One unintended and unforeseen consequence of the central bank intervention was that low interest rates left investors struggling to find higher returns. Many moved into the stock markets, where central bank purchasing and corporate buy-backs guaranteed rising prices. Others, though, gambled on “junk bonds” – highly risky investments where the risk of losing your money is far higher. One beneficiary of this search for yield was a American hydraulic fracturing industry which spent the next decade spending billions of dollars’ worth of investors’ cash to extract millions of dollars’ worth of “unconventional” (i.e. expensive and nasty) oil in such quantities that global oil extraction began to grow again.

At the same time, two developing economies – China and India – turned to an older and dirtier energy source – coal – to power global industrial civilisation’s final spurt of economic growth; just sufficient to prevent the entire system from imploding into an unstoppable collapse.

Then came what energy expert Kurt Cobb refers to as a stealth peak in world oil extraction:

“We who have been suggesting that a peak in world oil production was nigh almost from the beginning of this century looked like we might be right when oil prices reached their all-time high in 2008. But since then, we have taken it on the chin for more than a decade as the U.S. shale oil boom kept adding to world supplies—even as production in the rest of the world mostly stagnated or declined.

“But then world oil production turned down—not when the recent coronavirus pandemic and associated economic shutdowns hit—but more than a year before while few people were noticing. Monthly fluctuations will make it difficult to pinpoint a peak until long after it occurs. But, let’s note the difference between world output in November 2018 which was 84.5 million barrels per day (mbpd) versus December 2019 which was 83.2 mbpd when the world economy was supposedly still in high gear. (These numbers are for crude plus lease condensate which is the definition of oil on major oil exchanges.) Between these two dates monthly oil production was occasionally lower than December 2019, but never higher than November 2018.”

The economic consequences of this were already being felt long before SARS-CoV-2 embarked on its world tour. December 2018 was the worst Christmas on record for retailers until Christmas 2019 came around. Across the developed economies the growth of nationalist populism and outbreaks of social unrest such as the bitter French yellow vests protests made it increasingly difficult for the metropolitan liberal class to continue to pretend that because its standard of living had increased, so must everyone else’s. Even in China, where massive infrastructure investment had kept the global economy from entering a period of de-growth, collapsing western consumer demand was grinding economic growth to a halt.

The response to the pandemic has merely accelerated a process that had already begun. Instead of a gradual collapse across several years, we have witnessed a decline in economic activity – and a corresponding fall in energy use and carbon emissions – worse and more rapid than the Great Depression of the 1930s. And this is just the start. As the impact of the loss of purchasing power among the several million newly unemployed/underemployed households and newly bankrupted businesses filters through to the balance sheets of bigger corporations and on to the banks themselves, things will inevitably go from bad to worse. Add to this the impact of “coronaphobia” – consumers refusing to purchase from outlets like airlines, bars, cinemas and restaurants where there is still a high risk of infection; and, more devastatingly, investors refusing to put more cash into such enterprises – and we could well be facing the biggest economic crisis in the history of industrial civilisation.

Behind the scenes, the central banks continue to play their pacemaker role – propping up stock markets, reducing interest rates to zero and pumping trillions of dollars into the system – to prop up businesses and households until such time as governments can figure out (don’t hold your breath) how to get us out of this mess. The two – broad – solutions currently on offer might be referred to as a green new deal and a black (i.e. fossil fuel-based) new deal. The latter involves restarting an economically damaged oil industry and supplementing it with coal and gas by cutting regulations in order to kick-start another round of growth. The former envisages growth generated by installing non-renewable renewable energy-harvesting technologies on an eye-watering scale in order both to replace the energy from fossil fuels and to provide additional energy to grow the economy.

Both proposals fail for the simple reason that the energy available to power the global economy is in decline. This is not simply a matter of the amount of coal, gas and – especially – oil being extracted being in decline. Less obviously, it is about the increasing amount of energy required to extract these fuel sources. Ironically, one growing use of renewable energy is to lower the energy cost of fossil fuel extraction. Indeed, renewable energy is largely an extension of the existing industrial system rather than a replacement for it. As Mary Wildfire explains:

“…the generation of electricity is only about 20% of energy use. So even if we made a complete switch to those renewable energy systems, we would still also need transformations in transportation, agriculture, buildings, and the materials sector…

“Putting that aside, is it possible to switch all of our current generating facilities, now running on fossil fuels or nuclear power, to clean sources? We have to take into account that a sizable part of the human population still lacks any access to electricity, and most people feel that simple justice requires allowing them to increase their energy use to some decent minimum. Thus we need to replace maybe 125% of today’s generation capacity, to maintain current usage levels while adding this impoverished sector.”

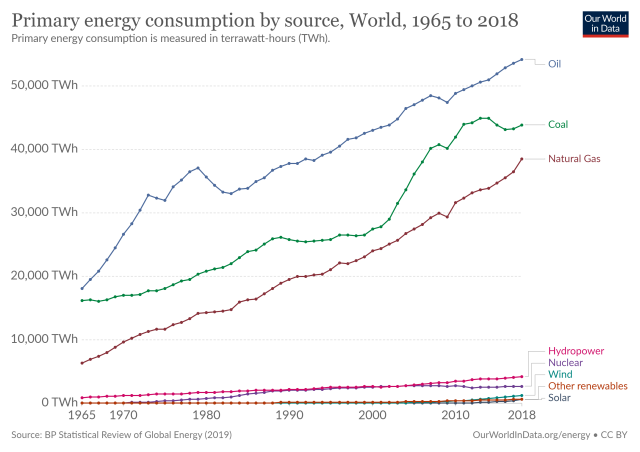

The harsh reality is that despite the Herculean deployment of wind turbines, solar panels and biofuel plants over the last three decades, fossil fuels still provide more than 86 percent of the energy that powers the global economy. Indeed, strip away hydroelectric power – since there are limited additional valleys left to dam – and remaining renewable energy accounts for just four percent of our consumption; most of it in the form of electricity which is more or less useless to our most critical (heavy) transport, agricultural and industrial needs:

This is the immoral and unpalatable (and thus glossed over in establishment media) aspect of the proposed green new deal – it amounts to a final imperial resource grab in which a handful of developed states use what remains of the value of their currencies to secure the last of planet Earth’s resources in one final economic blowout that will last right up until the first of the irreplaceable wind turbines and solar panels begin to breakdown. Après ce, le deluge…

There is simply no way in which the global economy gets to grow without fossil fuels – which, incidentally, are essential at every stage of the manufacture, transportation, deployment and maintenance of non-renewable renewable energy-harvesting technologies. The unspoken paradox of the green new deal is that you would need to double the fossil fuel that we currently burn to build, deploy and maintain enough non-renewables to replace the fossil fuel that we currently burn. And if you are going to do that, why not go for the simple black new deal being offered by politicians like Trump?

The simple answer is because we have now passed the peak of unconventional oil extraction too. The collapse in demand caused by the pandemic has hastened the process because closed down oil facilities and wells are much harder and more expensive to restart. As Philippe Gauthier explains:

“To the lay person, the option to cut production seems obvious. But an oil well is not a tap with a flow that can be adjusted as needed. Either it operates at full capacity or not at all…

“An oil field is a complex structure, where different grades of oil have settled over time in a porous type of rock such as sandstone. Drilling and pumping releases this mixture of oil and gas. Any cessation of the extraction process may result in the clogging of this porous rock with sediment or paraffin, which means that production may permanently be reduced by half, or even stop completely, when pumping resumes…

“Most refineries cannot operate below 60 or 70 per cent of their baseline capacity. A few select ones can go as low as 50 per cent, but no less. If oil production keeps decreasing, some refineries will have to close, temporarily or permanently. Production at US refineries has already fallen by 30 per cent, which means that they’ve already almost reached the shutdown point…

“Here again, we are talking about equipment which must continue operating as it will fall into disrepair when not in use. For some old and marginally profitable refineries it may therefore be financially impossible to resume operations after a shut down.”

With oil extraction already past peak, any attempt to return the global economy to its pre-pandemic level via the fabled “V-shaped recovery” is likely to generate oil shortages which could see prices temporarily rise above a depression-inducing $100 per barrel. No amount of central bank financial alchemy is going to add oil to depleted fields or remove the gunk from shutdown wells, pipelines and refineries. And so a black new deal can only occur by diverting a large part of the energy previously used in the wider economy to the extraction of the last of the accessible fossil fuels – in its way, essentially the same imperialism as the green new deal, in which a handful of people in a handful of wealthy states enjoy one last energy-consuming blowout before industrial civilisation crumbles to dust; except in this version we incinerate what remains of planet Earth through runaway global warming.

As Mary Wildfire puts it:

“Can we get real solutions and still maintain economic growth, population growth, and the growth of inequality? Are we entitled to an ever-rising standard of living? I believe the answer is no; we need some profound transformations if we are to leave our grandchildren a planet that resembles the one we grew up on, rather than a dystopian Hell world…

“A veritable cornucopia of false solutions is being pushed these days, not only by corporations and think tanks but by the UN’s IPCC, the international body responsible for research and action on climate. We could have made a gentle transition if we had begun when we first became aware of this problem decades ago, but for various reasons we did not. There is no time left for barking up one wrong tree after another; no time to waste in false solutions.”

If neither a green nor a black new deal is available to us, what is to be done? One answer is a kind of brown new deal based around a managed de-growth aimed at making the collapse of industrial civilisation as painless as possible. Such an approach does not claim any one energy source as better or worse than another, but rather aims to utilise the energy we still have available to us to simplify, regionalise and localise our economies as best we can in the time available to us. Nor does such an approach fit into traditional left v right political views which are all based upon the religion of progress and endless growth. Rather, it views a combination of the raw power of the state and the innovativeness of private markets to work together to create as soft a landing as possible.

The process begins by turning off the pacemaker – removing the central banking system and the creation of infinite volumes of debt-based currency – and allowing the cancerous financial sector of the economy to collapse back into line with a real economy which is already shrinking. Ideally, we would peg the amount of currency in circulation to the amount of energy available to the economy, while returning financialised social services such as childcare and preparing food to communities and families.

A proportion of the remaining fossil fuels (hence a “brown” new deal) would be used to deploy alternative energy generation, including wind and solar; but not with a view to growing the economy. Instead, the energy which remains to us would be redirected to maintaining pockets of complexity, such as some degree of socialised medicine or a functioning water treatment and sewage disposal system. Meanwhile, a great deal of the (often debt-based) consumption which has grown the financialised economy in the last three decades will have to go away. The word “enough” and the old wartime plea to “make do and mend” will have to feature large in the vocabulary of the future. Most work will have to be refocused on genuinely essential activities such as growing food and transporting essential commodities.

In this way, the elephant in the room – overpopulation – might be addressed without the need for a catastrophic cutting short of the lives of billions of people through war, pestilence and famine; as is the most likely outcome in the event that we are foolish enough to attempt either a black or a green new deal.

It goes without saying that the global elite – the 0.1 percent at the top who nominally own as much wealth as the bottom 90 percent – will resist any version of a new deal and will instead insist that the central bank pacemaker be kept running at all costs. But one way or another as with every baby boomer fitted with a pacemaker, this economy is going to die in the not too distant future anyway. The only question is whether it is allowed to go peacefully once the pacemaker has been switched off, or painfully as artificial stimulation fights against the traumatic organ failure which follows an energy supply collapse.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.