Related Articles

|

|

The trouble with “common sense” is that it is wrong more often than it is right. And today’s common sense – based on the experience of the 1970s – is that the massive volume of currency printed into existence in response to the pandemic is about to erupt into an inflationary crisis. This though, overlooks the many differences between the semi-autocratic national economies of the 1970s and the global economy of the 2020s.

The inflation of the 1970s is often wrongly attributed to excess government currency printing. But this is to mistake attempted cure for the crisis itself. As in 2008, the crisis of the 1970s began with the peak in US conventional oil production. The ensuing loss of control of global oil prices allowed the oil corporations and the OPEC cartel to jack up prices and to threaten the western economies with artificial shortages. The resulting higher prices – which filtered through into the price of everything made from or transported with oil – served to slam the brakes on economies which had been growing consistently throughout the post-war years. As historian Paul Kennedy explained:

“The accumulated world industrial output between 1953 and 1973 was comparable in volume to that of the entire century and a half which separated 1953 from 1800. The recovery of war-damaged economies, the development of new technologies, the continued shift from agriculture to industry, the harnessing of national resources within ‘planned economies,’ and the spread of industrialization to the Third World all helped to effect this dramatic change. In an even more emphatic way, and for much the same reasons, the volume of world trade also grew spectacularly after 1945…”

Common sense held that the economic conditions of the post-war boom were “normal,” when in fact they were an historical anomaly brought about by the once-and-done conversion of the European economies from coal to oil in the aftermath of the war. Nevertheless, even as late as the 1970s, those economies continued to support the institutions of a coal-powered economy. Prior to the 1986 “Big Bang” financial deregulation, national economies imposed strict capital controls in order to force investors to finance domestic industry. On the other side of the same coin, mass trade unions born out of coal-based industries like mining, steel working, railways and ship building, continued to exercise a powerful veto on industrial policy and practice.

Productivity – effectively the deployment of technologies to increase the exergy obtained from energy – had allowed workers to reap a far larger share of the profits than had occurred throughout the industrial age. Where in the 1920s, a worker on the average wage struggled to rent a small terraced home with basic amenities, the average worker during the boom could purchase a house, raise a family, run a car and take an annual holiday. The price rises of the 1970s threatened to bring those gains to an end. And so conflict broke out between investors and workers over the apportionment of the profits.

Both trades unions and investors went on strike. At the same time, governments which had become conditioned to intervening in the economy in the post-war years, sought to pour oil on these troubled waters by opening the printing presses and spending new currency into existence – a trick which appeared to have worked in the aftermath of the war itself. But it is one thing to generate massive volumes of new currency into an economy which has both massive slack – unemployed workers and stored up capital – and vast untapped energy and resources. It is another matter entirely to open the spigots when the economy is already at full employment and when energy and resources are in short supply.

Additional currency which, because of financial controls, had to circulate within national economies worked to raise prices – i.e., devalue the currency – across the economy. In addition, the USA’s establishment of an oil standard to replace the post-war gold standard allowed US inflation to be exported to its trading partners; who were obliged to buy oil in US dollars. And so, governments struggled both to curb industrial unrest and to quash inflation with varying degrees of failure prior to the collapse of the post-war consensus in the 1980s.

Helped by the influx of new – albeit more expensive – oil production in the North Sea, North Alaskan Slope and Gulf of Mexico, the Reagan and Thatcher governments had been able to shift the key focus of government policy away from full-employment to sound money and stable prices. The ensuing unemployment helped to finally break the backs of the coal-based mass trade unions; while the relaxation of financial controls opened the way for the debt-based casino economy of the 1990s and early 2000s. What could possibly go wrong?

Importantly, few of the conditions which fed into the inflationary crisis of the 1970s are present in the post-pandemic world. Trade unions are largely impotent in the face of deregulated global finance. As they have learned from bitter experience since the early 1980s, industrial disputes and strikes most often result in the offshoring of their members’ jobs. In the European Union, for example, a determined employer could dismantle a car assembly plant in, say, Spain and move it to Slovakia in the course of a long weekend. The unions would be left picketing an empty warehouse. In reality, few need contemplate such action because it was already taken in the form of offshored supply chains in the 1980s and 1990s.

It goes without saying that capital is no longer national, and may disappear faster than it arrived. As historian David Edgerton observes:

“Today there is no such thing as British national capitalism. London is a place where world capitalism does business – no longer one where British capitalism does the world’s business. Everywhere in the UK there are foreign-owned enterprises, many of them nationalised industries, building nuclear reactors and running train services from overseas. When the car industry speaks, it is not as British industry but as foreign enterprise in the UK. The same is true of many of the major manufacturing sectors – from civil aircraft to electrical engineering – and of infrastructure…”

Since the 1980s, capital has been free to move to wherever in the world it can secure the greatest rate of return. Allegiance to nation only exists so long as states resist the temptation to hike taxes and to impose new regulation. And the “beneficial” consequence of this for western consumers is that the prices of consumer goods and services are driven down accordingly.

Beyond these changes in the real economy, in the years since 1980 a cancerous financial system has metastasised to suck the life out of anything which attempts to return to a free market based on manufacture and trade. Today there is an almost closed loop within which central bank reserves and government bonds are used to contain new currency within a series of asset bubbles – stocks, property, fine art and collectables, etc., from where they cannot escape to cause inflation across the wider economy.

This massive explosion of nominal “wealth” at the top mirrors the ebbing tide of prosperity at the bottom. The old, relatively well-paid working class has been largely replaced by a burgeoning precariat working in low-paid self-employment, part-time jobs and zero-hours contracts. Where giant steel works, ship yards, railway depots and mines dominated the labour market, today’s fragile employment is within shopping malls, hotels and restaurant chains. Only in a few shrinking pockets around the top-tier universities and financial centres do we find enclaves of prosperous, salaried employment.

It is into these new conditions that massive volumes of pandemic-mitigating currency are now flowing. And it should go without saying that the majority of the new currency is still flowing into the various asset bubbles that substitute for profitability in the post-2008 economy. But still, sufficient volumes of new currency have been used to prop up or replace wages for the spectre of inflation to be taken seriously. Although there are both psychological and structural reasons to believe that collapsing profitability is going to be a bigger issue than inflation… at least in the short-term.

Price increases are of course, inevitable as a result of the active sabotage of the global, just-in-time supply chains which used to serve to drive costs down. Production processes have been shut down – some never to reopen – ships have been scrapped, and shipping containers are lying idle in the wrong ports. Migrant workers too, are no longer available to employers in the big cities; where they provided far cheaper labour than indigenous workers who insist on the minimum wage. During the pandemic, for example, London experienced a haemorrhage of Eastern Europeans, who decided that it was safer and easier to ride out the pandemic at home than to remain in the cramped and shared accommodation provided by spendthrift employers. One consequence has been that as Britain began to unlock in April, said employers were unable to recruit cheap enough workers.

The common sense expectation here is that this will fuel inflation because workers have the upper hand and will force businesses to increase wages. This though, ignores half a century of economic history. In the 1970s, for example, eating out was largely a pastime of the salaried classes. Working people did it very occasionally; on special occasions like anniversaries. And when they did, the fare on offer would be considered a joke by today’s standards. The reason that – at least prior to 2008 – ordinary people have been able to enjoy quality food at a relatively low price, is precisely because these businesses have driven down the cost of everything from rent and labour to the quantities of salt and dressing provided with each meal. In short, in business across the retail and hospitality sector, there is no possibility of raising wages to meet shortages without undermining profit margins… closure is the only option.

The same is true for the many materials which are in short supply as a consequence of the response to the pandemic. Things as ubiquitous as a microchip or a fuel derived from oil might be expected to increase in price as businesses and consumers compete to obtain them. And in the short-term, this is happening. But in the longer-term, it is the ability of consumers as a whole to purchase, rather than the needs of businesses to remain profitable which will win the day.

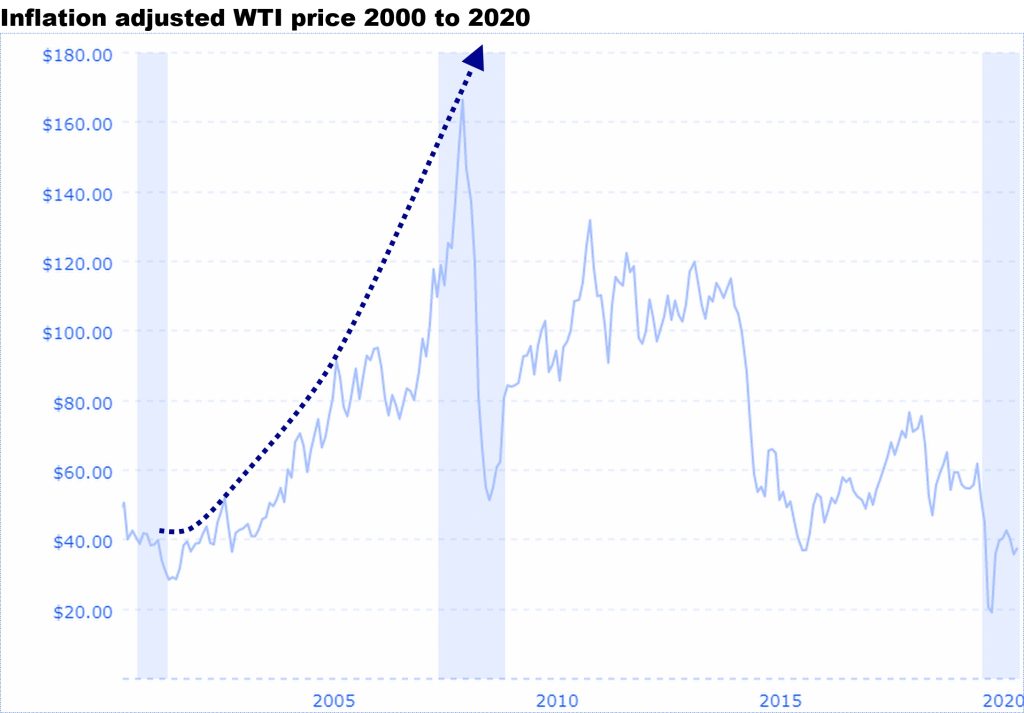

We have already seen this occur with oil in the years since 2008. After the big increases in oil prices either side of the crash, in 2012 Michael Kumhof and Dirk V Muir from the International Monetary Fund published a paper anticipating $200 per barrel oil by the end of the decade. Given what had been happening around that time, the proposition appeared entirely plausible:

But that wasn’t how things worked out. For sure, the cost of producing oil had risen dramatically following the global peak of conventional oil extraction in 2005. There was plenty more oil to be found, but it was in expensive to produce deep sea, tar sands and shale deposits. Oil companies need prices of $200 or more to keep increasing the global yield; but prices collapsed after 2015:

Importantly, in the years since the financial crash, there has been a widening gap between the average wage so beloved by the establishment media, and the less mentioned median wage; the halfway point on the income ladder. In the UK just prior to the pandemic, the average wage was nearly £6,000 above the median; reflecting the growth of the low-paid precariat and its downward drag on the lowest-skilled employment sectors:

A similar, pre-tax $10,000 gap can be seen in the USA, reflecting the growth of low-paid employment in that economy since the crash.

As Gail Tverberg at Our Finite World has argued on many occasions, the key driver in the modern economy is the lack of aggregate consumer spending power. In the 1990s and early 2000s, this was hidden via a combination of offshoring – to lower the wage bill – and wider access to debt – to allow western consumers to keep buying. This was the system that imploded – and should have been allowed to reset – in 2008. Since then, governments across the developed economies have been playing a game of extend and pretend in which rising stock and bond prices are used to mask the decline in prosperity which was already fuelling a retail apocalypse long before SARS-CoV-2 embarked on its world tour.

There is no reason to believe that the rising prices brought about by pandemic-related supply-side shocks will follow a different course. That is, initial price spikes caused by businesses attempting to pass increased costs onto consumers, will be met by swings in consumer spending away from discretionary items in favour of essentials. As a consequence, businesses in the larger, non-essential, sectors of the economy will experience rapidly falling demand. If they still have some cost-cutting capacity, they may attempt to stay in business by such things as re-financing debt, renegotiating rent and cutting their wage bill. But these, of course, serve to lower aggregate consumer demand – and generate a psychological wariness of new spending or borrowing – making the problem worse. And many businesses have already taken these actions in response to the pandemic.

When the UK economy began to unlock in April, the banks and the establishment media desperately tried to talk up a consumer-driven boom. The stark reality, in contrast, is that tens of thousands of businesses have already gone to the wall, and hundreds of thousands of workers are unemployed; with as many again only nominally employed for so long as the state keeps underwriting their wages. One in seven shop fronts on Britain’s high streets failed to open when the lockdown ended, because they had already gone bust. According to the Centre for Retail Research, 5,214 stores employing 109,407 people went bust in 2020 despite the unprecedented levels of support available from the government. A further 1,663 employing 25,154 people went bust in the four months to April 2021. These figures exclude non-UK businesses and restaurants, cafes and food services.

The point is that while there may be a brief period of letting off steam following the lockdown – as happened last year – it is likely to be short-lived – as happened last year – at least so long as businesses are closing, the media are continuing to whip up fear about new virus strains, and governments continue to maintain emergency powers to throw the economy into reverse at a moment’s notice. In such circumstances, people are likely to use any savings they’ve accumulated as a cushion against the next crisis rather than dash out on a spending spree.

The idea that there is sufficient pent up savings in the economy to generate an upturn on a par with the post-war boom is simply fanciful. Too much of the savings are locked up in the accounts of the wealthy, while too much of the outstanding debt is a burden on the lower than average-paid workers at the bottom. Rich people may have savings, but there is no reason to expect them to dramatically increase their spending to make up for the massive loss of spending power at the bottom. Most likely, when the various forms of government stimulus come to an end, and the newly printed currency finds its way back to the stock and bond bubbles, we will experience a period of stagnation as businesses which can no longer make serious cuts to their operating costs die on the altar of supply-side shortages. And as unemployment and under-employment increases, so the contagion will spread. For example, shop and hospitality closures result in falling commercial property rents which, in turn, drive pension funds toward bankruptcy. And just as nobody could know in advance which goods would be affected by supply chain disruption, we cannot know in advance which businesses will fail in the face of rising costs and falling demand. What we can say though, is an awful lot of the nominal wealth locked up in bonds, shares and the other giant asset bubbles will evaporate in the face of the coming crisis of profitability.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.