Related Articles

|

|

One of the consequences of the response to the pandemic and the disruption from Brexit is that labour shortages are appearing across the low-paid sectors of the economy. So much so that even the metropolitan liberal Guardian has begun to wonder whether the benefits of higher wages for the low-paid might outweigh the cost of having to pay more for a plumber or an au pair. As John Harris puts it:

“For decades, large swathes of the labour market have been run on the assumption that there will always be sufficient people prepared to work for precious little. But here and across the world, as parts of the economy have been shut down and furlough schemes have given people pause for thought, the idea that they need not stay in jobs that are exploitative and morale-sapping has evidently caught on.

“In the UK, meanwhile, Brexit remains a disastrous and chaotic project – but, among its endless and unpredictable consequences, leaving the EU has cut off employers’ access to a pool of people who were too often exploitable. Time has thereby been called on one of the ways that our dysfunctional labour market was prevented from imploding.”

Harris points to sectors of the economy – mostly low-paid – where employers have been obliged to increase wages in order to fill vacancies. And there is certainly some room for wage increases across the economy. But the emerging narrative is that this is a bad thing because it will create price increases. Much of the thinking around this issue though, is based on experiences and on economic models that last saw the light of day half a century ago. And with this in mind, we should take mainstream narratives with a pinch of salt.

One problem is with the definition of “inflation,” which has changed beyond recognition in the last few decades. Initially, inflation referred solely to the inflation of the currency – price rises were a symptom rather than the disease. But today, price rises – which can occur for many non-monetary reasons – are considered to be inflation. This is a particular problem at a time when governments around the world actually have massively inflated the currency because it is too easy to assume that any subsequent price increases must be the result of monetary policy. As happened between 2005 and 2008, treating price increases as synonymous with inflation, while failing to understand the underlying weakness of the economy, resulted in monetary policies which turned a temporary slowdown into a global collapse of the banking system. The same mistake might easily be repeated as the world economy struggles to emerge from the various responses to the pandemic.

Prices are certainly rising. The price of oil is nearly double – $75 per barrel – its March 2020 price. And since just about everything in the economy is either made from or transported with oil, that is likely to temporarily drive prices higher across the economy. But it would be extreme stupidity for governments and central bankers to raise interest rates and implement austerity cuts while national economies are still reeling from the various lockdowns and restrictions which have disrupted the world’s just-in-time supply chains. As J.W. Mason at the Roosevelt Institute explained in an interview with Intelligencer:

“Inflation, right at this moment, is exactly two things. We’re seeing a big increase in the price of fossil fuels, gasoline, obviously, but also heating oil and so on. That’s one. And two, we’re seeing an increase in the price of automobiles, which is driven, I think, by some degree of supply chain issues plus pent-up demand. And that’s it. That is 100 percent of what we are calling inflation today. Neither of those phenomena has anything to do with the money supply. They have to do with factors specific to those particular two sectors of the economy. It doesn’t mean that they are not important, or that they don’t impose hardship on people who are paying those higher costs. But to think of this as somehow being related to something about money printing or the deficit, it’s just silly. And in any other context, we would recognize that whatever is setting the price of used cars, it’s not the Federal Reserve or the federal budget. It’s something specific to that industry.”

Economic models – which only exist to make astrology look good – are so simplistic that they fail even to tell us who or what determines prices in the real world. As Mason argues:

“I think there are three questions we should ask about all this. One is: Is it actually the case that labor markets are so tight, they’re generating very large wage increases? And that’s an empirical question. We can debate that. The second question is: Is unemployment unsustainably low, in the sense that we are trying to employ more people than the economy has available? And the answer is absolutely not.

“But the third question is: what actually happens when you have accelerating wage increases? The assumption of the textbook story is that 100 percent of workers’ wage gains get passed on into prices. The idea being that prices move up and down in lockstep with wages. And there’s absolutely no reason to think that that’s true. In fact, there’s overwhelming evidence that it is not true. The textbook story just assumes that the division of income between wages and profits can never change.”

It is not the case – as anyone who has actually had to meet a wage bill can testify – that wage increases automatically translate into price increases. Companies often absorb costs by cutting operating costs and/or eating into profits. This is especially true in sectors of the economy which require high volumes of low-price sales to remain profitable.

Nor does the simple assumption that inflating the currency supply must result in higher prices, stand up to scrutiny. After all, since the 2008 crash, central banks around the world have been using monetary policy to inflate currencies in an increasingly desperate attempt to make inflation rise to the pre-crash preferred level of two percent. And prior to the pandemic at least, the policy failed spectacularly.

One reason, of course, was that the newly generated currency was funnelled directly into the hands of the big corporations and the already wealthy. While the bottom half of the population have taken a cut in living standards since 2008, the wealthy have had their mouths stuffed with gold… or at least quantitative easing and lower than inflation loans. Insofar as monetary inflation exists, it is in the places where wealthy people put their money – in inflated bond markets and stock markets that no longer bear any relationship to the value of the listed companies; in the eye-watering prices of fine are, luxury goods and collectibles; and in the voracious hedge fund takeovers of everything from football clubs to supermarkets.

Nevertheless, the “wage-price spiral” that they hoped would kick-start another round of economic growth stubbornly refused to materialise. And even now, despite shortages of goods and labour, it is far from clear that price rises will be more than short-term or that a general rise in prices is about to set in. A key reason for this is that the few wage rises that have occurred involve competition for labour between companies in particular industries such as road haulage and restaurants. Increasing the wages of a handful of chefs and drivers, poached from a competing company, does not serve to increase the consumption of the entire population. Companies which raise wages may attempt to raise prices to compensate, but doing so risks losing sales and thus losing money.

Viewed from an energy-based perspective, the issue is far more profound. The reason we currently have shortages of both goods and labour is simple enough to understand. In response to the rising energy cost of energy from the 1970s, companies sought to pare their operating costs to a minimum. Where cheap labour was available – such as within the European Union after the former Warsaw Pact states were incorporated – this could fill shortages and drive down wages at the bottom of the income ladder. Where cheap labour was unavailable, operations were moved to parts of the world with cheaper labour and fewer workers rights. The same was done with materials and resources, using just-in-time supply chains to cut storage space and to lower prices.

If the energy cost of energy had stabilised at 1990s levels, these new arrangements might have continued indefinitely. Bernanke’s “Great Moderation” might have continued indefinitely. And the New American Century might have been realised. But the rising energy cost of energy is remorseless. Absent a new, even more energy-dense than diesel source of power, economies around the world were thrown into reverse from the early 2000s; with the most complex economies experiencing slowdowns first. Far from defeating the Soviet Union in the Cold War, the USA was just a couple of decades behind it in falling apart. The economists and central bankers had not put an end to the cycles of boom and bust, they had merely built a mountain of unrepayable debt to paper over the cracks. And if the twenty-first century was to be the property of any one empire, it had a distinctly Chinese flavour to it.

In 2005, global conventional oil production peaked. The ensuing rise in prices across the economy as businesses sought to pass on their increased fuel costs, raised the spectre of 1970s-style inflation. Like generals fighting the last war, the central bankers raised interest rates so that the mountain of debt they had created became even more unrepayable. Mortgage-payers who had just about been managing to make their payments were thrown into arrears, and the world learned about “sub-prime lending.” And then it turned out that the entire global banking system was a Ponzi scheme which depended upon the income from sub-prime mortgages to stay solvent. And when it all came tumbling down, the politicians generously put their hands into our pockets to bail out the rotten system.

In a kind of reverse Robin Hood, the various measures taken to maintain the banking system – quantitative easing, below-inflation interest rates, public austerity cuts, etc. – transferred even more wealth from the poor to the rich; which is why statistics based on averages have become next to useless. A small number of ultra-wealthy people at the top serve to skew averages upward; giving the impression that economies are far more prosperous than is actually the case. In the UK, for example, the average wage – total wages divided by the working population – is more than £6,000 higher than the median wage – the halfway point on the income ladder. Inflation – a shopping basket of goods based on average national consumption – is similarly distorted because the cost of essentials like housing, food, energy and transport which we all have to pay for, have risen far more than the discretionary consumer goods enjoyed by those in the top half of the income scale.

The “retail apocalypse” is the most obvious manifestation of this shift in income and wealth in favour of the already wealthy. Less obviously, the energy companies are caught in an “energy death spiral” as rising costs are forcing poorer households to self-disconnect (either not using energy at all, or cutting use to a bare minimum). The only available response – raising the price for the remaining bill-payers – serves only to encourage further self-disconnection. The growth of online retail is, similarly, a response to shrinking prosperity. By escaping the rental fees on city centre properties, the staffing costs of a physical store and the taxes levied on bricks and mortar businesses, online retailers have cut the cost of trading to a minimum. To hard-pressed consumers, this allows the purchase of products without all of the overheads. In short, when companies like Amazon are thriving, it is a sure sign that the broader economy is tanking.

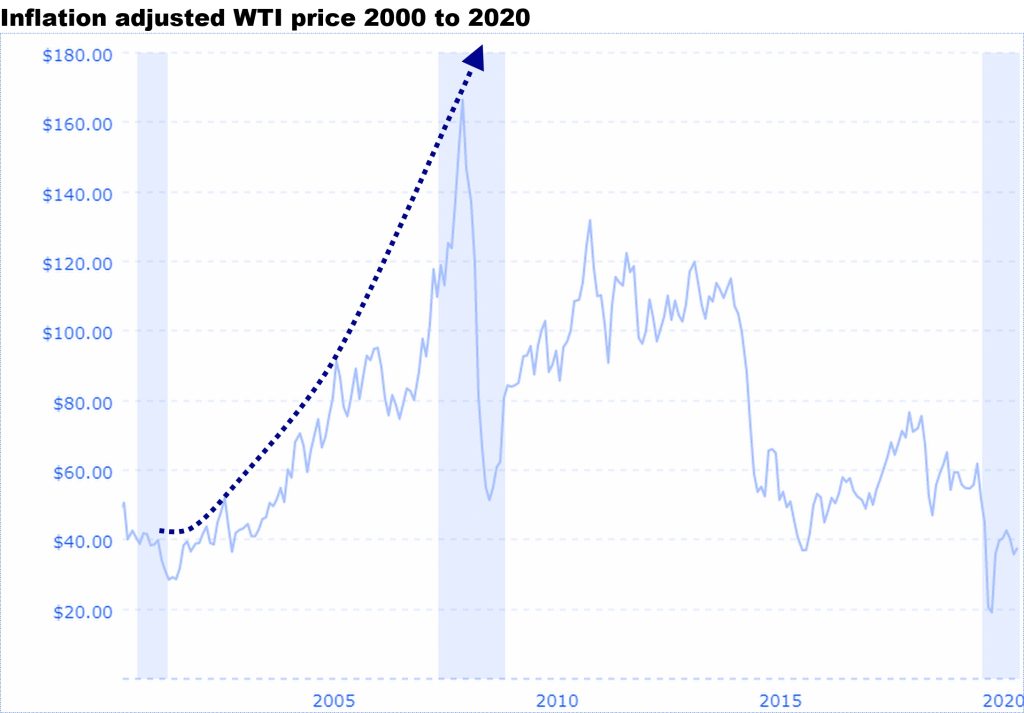

When conventional oil production peaked in 2005, the mainstream view was that oil prices would have to rise to $200 per barrel by 2020. This was the only way, it was thought, in which production growth could be maintained; allowing the oil companies to open previously unprofitable oil deposits. But that isn’t what happened:

Demand for oil slumped during the recession which followed the 2008 crash. And rising prices between 2010 and 2014 served only to halt further economic growth in its tracks. Relief of sorts arrived in the shape of the US fracking bubble in which companies spent billions of dollars of investors’ funds to produce millions of dollars’ worth of oil. In the artificial environment of quantitative easing and low interest rates, the frackers had been able to flood the global economy with oil which sold at far less than it cost to produce. Nevertheless, it was sufficient to bring global prices down to a point at which a degree of anaemic economic growth became possible once more.

Less obviously though, the entire period since 2010 has witnessed a price battle between oil companies and consumers which neither side can actually win:

The competition is not direct, of course – few consumers would want an unrefined barrel of crude oil. Rather, it is when the rising price of oil feeds into the rising price of everything made from, made with or transported using oil that consumers have to make some hard choices about what they are going to buy and what they are going to leave on the shelf. This is where the distinction between essential and discretionary spending is important. We have little choice other than to pay for essentials like food and clean drinking water, and so if the price rises, we must adjust our spending accordingly. In the end, this means that we must spend far less on discretionary items like holidays abroad or meals out at restaurants.

This is a problem for the economy as a whole because throughout the period since the Second World War, discretionary spending has been the main engine of economic growth. It is a problem for governments too, since most of their tax take is also from the discretionary sectors of the economy. And it is, of course, a nightmare for oil companies which are running out of oil reserves which can be extracted at a price the economy will bear – which is one reason why all of the big oil companies have been investing heavily in state-subsidised non-renewable renewable energy-harvesting technology projects.

Global peak oil passed almost unnoticed in 2018. The response to the pandemic, and to a much lesser extent Brexit in the UK, will undoubtedly accelerate the declines in discretionary spending which were already evident in the years between the Crash and Covid. Any talk of a Great Reset or Building Back Better is fanciful without the energy with which to power it. And no wishful thinking about wind, solar and hydrogen will change the physics and chemistry which make these entirely inadequate for powering an oil-based, global industrial economy.

In an expanding economy, corporations set prices because previously untapped energy and resources can be brought online to generate sufficient growth the make the higher price affordable. Moreover, productivity gains and competition will serve to bring prices down again. This is why, for example, the first colour TVs, computers and smartphones were only affordable to begin with to a handful of people at the top. But over time, prices fell until they were affordable to most of us. But note that it was still companies rather than consumers which set the price. Our current error is to believe that these processes – which only apply in energy and resource rich economies – also apply to our current energy and resource constrained planet.

In an energy-constrained economy like ours, it is consumers rather than corporations, governments or central banks who set prices. This is because as prosperity recedes, the majority of us have no choice other than to switch our spending from discretionary to essential items. And as the world begins to struggle out of the lockdowns and restrictions imposed by governments in the face of the pandemic, we will likely see the results of this on a grand scale.

Shortages resulting from lockdowns, together with rising energy prices are anticipated by governments, central banks and economists to be the early stages of an inflationary wage-price spiral. This though, assumes that companies will be able to pass those prices on to consumers. This is unlikely other than in the case of essential items such as the recent rises in energy, food and fuel. And even here, consumers still have choices – turn down the thermostat, buy chicken instead of beef, and walk rather than drive. Increased prices in discretionary sectors like restaurants and tourism simply invite consumers to shop elsewhere. And when the cost of doing business is greater than the income from sales, the result is going to be bankruptcy.

Since everything in the economy depends upon energy, and since the energy cost of energy is rising and can no longer be brought down, then we know that theoretically the economy must shrink. We also understand that this forced de-growth is likely to begin in the discretionary sectors of the economy. And because in a shrinking economy it is ever less prosperous consumers rather than businesses who set the price, we look set to see a wave of bankruptcies rather than a wave of inflation in the near future.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.