Related Articles

|

|

It is of some interest that people have been contrasting images of British petrol queues this weekend with the petrol queues which formed back in 1973 as a result of the OPEC oil embargo. Not least because a more accurate comparison is with the fuel protests in September 2000. That is, this weekend’s “shortages” are largely the product of a multinational oil company launching a media campaign aimed at avoiding having to improve the pay and conditions of its drivers. From past experience – including your rush to get toilet paper last March – you didn’t have to be a genius to realise that publicising a faux shortage of fuel would lead to a run on the country’s filling stations. They are, after all, just like banks in that if we all turn up at the same time, they break. And so, in a matter of hours fuel shortages became a self-fulfilling prophesy; aided by ministers taking to the airwaves to urge people not to panic.

If anything, we have become even more dependent upon just-in-time deliveries today than we were 21 years ago. And back then it only took the loss of 15 percent of deliveries to bring us to the brink of a cascading collapse. This is because the real economy fails in the same way as Liebig argued that crops fail. The absence of one component is sufficient to bring about a total failure. So, for example, in September 2000 several English hospitals ceased treating people because of a shortage of Sucher. The operating theatres were ready to go. The surgeons were in place. The patients were ready to be anaesthetised. But without the means of stitching them back together, the entire process had to be put on hold. Across the economy, systems began to fail in the same way leading to fears that critical infrastructure such as the electricity grid or the water and sewage system might fail.

The 1973 shortages were a different matter because there was nothing internally artificial about them. Although in part a reaction to the western intervention in the Arab-Israeli War (which explains the timing but not the underlying reason) the OPEC sanctions were largely a response to the peak of US oil production three years earlier. Prior to that point, the Texas Railroad Commission had exercised control over global oil prices by increasing or decreasing output. Once passed peak though, they could no longer raise output to hold prices down. This suited both the Middle Eastern oil states and the multinational oil companies, who could now force prices up. And the demands were forced home by the imposition of an embargo upon economies which depended on oil for their existence.

Internally, countries like the UK got their first taste of what a world afflicted by declining oil production would be like. And it was not just the immediate rationing of fuel and problems moving goods around. The increased oil price fuelled the stagflation of the period by driving up the price of everything made from, with or transported using oil, while simultaneously lowering the profitability of every business sector of the economy.

It is no accident that the mid-1970s saw increased interest in environmental issues and in potential alternatives to fossil fuels in general and oil in particular. Although a conspiracy theory common at the time may have lulled us into a false sense of security – this was that Big Oil had bought up the patents on a series of energy technologies that did not need oil, and that these would be developed once the world faced a production peak. It turned out that the best they could offer was wholly inadequate wind turbines and solar panels which require fossil fuels at every stage in their manufacture, transportation, deployment and maintenance.

What the higher price of oil did do, however, was make the previously too expensive deposits north of Alaska, in the North Sea and the Gulf of Mexico worth bringing into production. And it was these (and the money-laundering based upon them) – rather than the maniacal economic policies of the Thatcher government – which finally turned the economy around by the early 1990s. Globally, Clinton’s debt-based expansion of the currency supply – mirrored by Blair in the UK – helped usher in the decade of unsustainable debt-based growth which came to grief in 2008. And yet again, our narratives get this crash wrong by blaming immediate political issues rather than long-term resource limits. For the political right, 2008 was the result of profligate governments borrowing and spending more than they could afford. For the left, it was down to greedy bankers and tax-dodging corporations running the financial system into the ground and then begging for state handouts.

While there is a grain of truth within these myths, as with the 1970s, the crisis began with resource depletion. The UK was particularly badly hit because its North Sea oil and gas reserves had been squandered by the end of the twentieth century. Both oil and gas production peaked in 1999 and fell rapidly thereafter. By 2005 the UK had become a net importer of oil and gas. Also in 2005, global conventional oil production peaked, with a similar impact to those experienced in the early 1970s. The price of everything that depended on oil began to rise.

The correct response to this should have been to do absolutely nothing. It was one occasion where “leaving it to the free market” would have done the least harm. Why? simply because in a supply-side shock, people have no choice other than to adjust their spending accordingly. This means less spending on discretionary items – such as electrical goods, new cars, holidays abroad or meals out – and more on essentials – like food, housing, utilities and clothes. The resulting decline in the discretionary sectors of the economy will result in bankruptcy for the least efficient leading, in turn, to a decline in demand for oil. Ultimately, the price of oil will have to settle at a price the economy can afford.

This is especially important to understand when dealing with an economy which has been overloaded with debt. In 2005, the overwhelming majority of economists, government advisors and ministers laboured under an entirely mistaken understanding of how the banking system works. They bought into models that assumed banks were the same as credit unions – relying on savers to provide the money loaned to borrowers, and making a small profit on the marginal interest rates. In reality, banks had been licenced to create a form of currency called “bank credit” – which is all of the digits that appear on your bank statement. By 2005, bank credit accounted for more than 90 percent of the currency in circulation. And every penny and cent of it had been spirited into existence when banks issued new loans.

The entire banking system was – and remains – a complex version of a Ponzi scheme; because in order to repay the interest on the currency already in circulation, we have no choice than to keep borrowing. Indeed, because compound interest grows exponentially, we have no choice but to borrow exponentially if we are to avoid a collapse of the global banking and financial system. But there are limits on the extent to which banks can keep lending. And arguably, we reached those limits in the early 2000s, when banks began providing mortgages to people who could barely afford to service them – the so-called “sub-prime borrowers.” Of course, the banks had taken measures to protect themselves from bad debt. Nevertheless, defaults at the base of the pyramid would bring the entire structure tumbling down.

Few people have examined the problem from the bottom up. But imagine yourself in the position of a sub-prime mortgage payer. The wider housing market has been dysfunctional for years. Monthly rents have risen far higher than the monthly repayment on a mortgage. But despite this, unless you can put down a large deposit – which is more or less impossible because of the high rent – you have no chance of getting on the housing ladder. But in the late 1990s, the banks’ voracious search for new borrowers reaches the point where you can get a 100 percent mortgage. And if you are careful – and prepared to move home regularly, you can use the rising price of each of the properties you borrow against to build the deposit on your next house. And eventually, rising house prices will allow you to pay off your mortgage entirely. That, at least, was the theory. And so you sign up for a mortgage that, provided you scrimp and save, you can just about repay. And then in 2005, prices across the economy begin to rise with the rising price of oil. By 2006, this is beginning to hurt because the cost of having a job – running a car, buying lunch, purchasing new work clothes, etc. – has left you with no discretionary spending. Still, so long as nobody does anything imbecilic, such as raising interest rates, things should settle down in future.

Unfortunately, raising interest rates is exactly what the economics textbooks recommend as a universal cure-all for rising prices. The fact that the rising prices – then as now – have absolutely nothing to do with the cost of borrowing is not even considered. And so those sub-prime borrowers who were just about keeping their heads above water were hit with the additional cost of increased interest payments. And these were the straw that broke the camel’s back. Borrowers began to default and the value of the banks’ securities began to plummet. And we then discovered that the banks had been setting up subsidiary companies to buy up their dodgy securities in order to keep the price up. And so, the banks stopped trusting each other and stopped all short-term lending to one another – the so-called “credit crunch.”

Oil supply and bad economics, not (or at least not primarily) greedy bankers or profligate governments, was the cause of the 2008 crash and the ongoing retreat of prosperity in the developed states ever since. And if you think that’s bad news, consider that global production of oil including unconventional sources – shale fracking and tar sands – peaked in 2018; although the full effects of this were hidden to some extent by the fortuitous arrival of SARS-CoV-2.

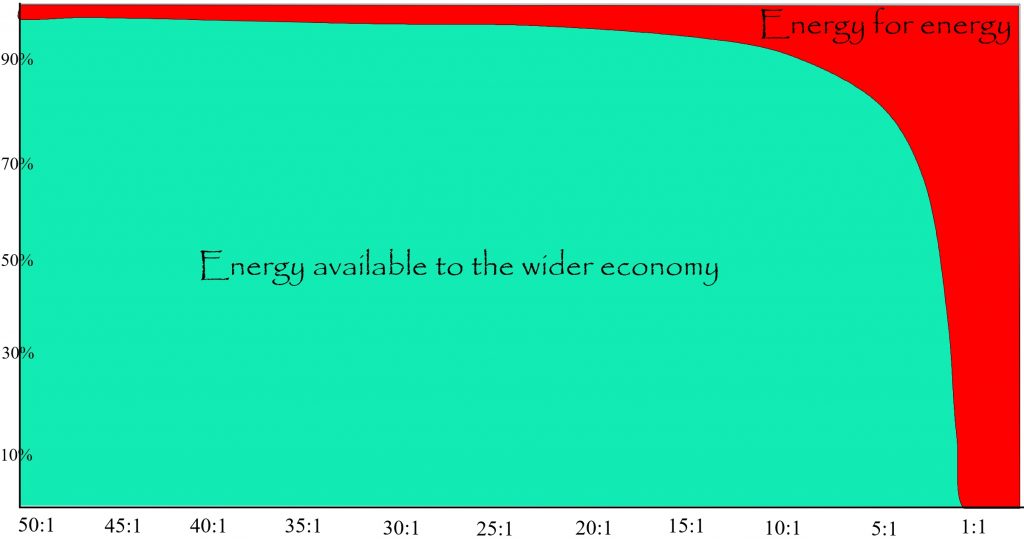

To be clear here, “peak oil” does not refer to the point at which we “run out” of oil. Rather, it refers to the last time ever that oil production grew. From now on, we will produce less oil than we did the year before. And because oil is a finite resource, we can do nothing to reverse the process. Nor is this a new discovery. Indeed, peak oil was theorised back in the 1950s and began to be taken seriously following the oil shock of the 1970s. Because, while you might be tempted to view oil as just another cheap resource, costing less than .50p per litre, the value we derive from oil is immense. And so, any decline in the quantity of oil available to us leaves us with some hard decisions about which sectors of the economy we will maintain and which we will have to bring to an end.

Worse than this though, the quality of the oil we rely upon has been declining too. That is, whereas we used to be able to extract oil by hammering a pipe a few metres into the ground, we now resort to strip-mining and cooking tar sands or hydraulically fracturing the source rock. And what that adds up to is a rising energy cost of energy as we are obliged to divert an increasing share of our energy into securing energy for the future. As a result, portions of the much larger non-energy sectors of the economy have to come to an end. And rather like Hemmingway’s character in The Sun Also Rises, this happens in two ways – “gradually, then suddenly:”

Each year since 1973 has involved a gentle slipping along the gradual downward slope toward the net energy cliff. Propped up to some extent by the last of the economically affordable oil deposits and disguised to a large extent by a mountain of unrepayable debt and over-inflated assets (sic), we fooled ourselves into believing that the crisis had gone away. Instead of treating the oil shock as a wake-up call, we lulled ourselves back to sleep in the mistaken belief that clever people somewhere else were dealing with it.

The 2005 oil peak and ensuing financial meltdown ought to have motivated us to take action too. But short-term political point scoring proved far more comforting than facing up to the predicament we were in by that time. In any case, the “fracking miracle” – which was largely a product of a desperate “search for yield” in an ultra-low interest rate financial environment – appeared to mean that our energy worries were behind us. Instead, climate change seemed to be the more immediate crisis.

Eight years after the crash, with little done to improve the lot of the bottom half of the population, and with prosperity retreating to a few enclaves near to centres of government, tech and the top-tier universities, the rise of right-wing populism should have been a surprise to nobody. Nevertheless, the advent of Brexit in the UK, Trump in the USA and the various post-Soviet eastern European nationalist populists have caused the political left to lose its collective mind. And, crucially, to unrealistically fantasise about restoring the status quo ante rather than addressing the growing crises before us.

The faux petrol shortage this weekend proved to be an excellent distraction from the far more serious gas shortage which was in the headlines at the start of the week. We are not, at this point, about to run out of fuel simply because developed capitalist economies don’t do shortages; we do price rises. Petrol prices in the UK are back to a level last seen in 2013 – which was the previous record high. That means that, as in 2005, people will be juggling their budgets and cutting their mileage to make ends meet. And when demand falls off, the oil price will begin to come down again; although perhaps no longer falling below the $40 per barrel that marks the upper boundary for economic growth:

Gas, on the other hand, really is running out… at least where Europe is concerned. Claims that the UK’s problems are the result of Brexit are precisely the kind of wrong diagnosis which leads to yet more quack remedies. Of course, as with the response to the pandemic and the closure of the Rough storage facility, Brexit will have had a minor impact. But the main difference between the UK and its European neighbours is that we took renewable energy far too seriously. That is, by over-building intermittent generation before we figured out how to store energy for times when the wind isn’t blowing and the sun isn’t shining, we left ourselves particularly vulnerable to fluctuations in the gas market. Despite the greenwash rhetoric, Germany maintained its coal power plants while Belgium and France kept their nuclear plants running beyond their expected lifespan. The UK in contrast actively closed coal plants and allowed nuclear to be retired so that gas became the only means by which we could balance the intermittency from wind.

This would have been foolish enough anywhere in the world. But in a northern country which also depends upon gas for home heating and cooking as well as for much of what remains of its industry, it was positively insane. There again, Britain’s wholesale energy market was designed to be insane from the beginning because its sole focus was on keeping prices artificially low for consumers – which is why a host of energy supply companies with unrealistic business models have been crashing in recent years. We can’t it seems have our electricity back-up and heat our homes with it too. Nor, having closed our mines and coal power stations, can we afford to go back.

The problem with misdiagnosis is that it leads us down paths that will make matters worse in the longer-term. If, for example, you were to conclude that the solution to our growing energy crisis is to re-start attempts at fracking, you are going to waste a lot of our remaining resources trying to create an industry which has been shown to be energy-negative – in the UK, because of our twisted geology, shale gas simply cannot be extracted for less energy than is produced. Which is why, of course, the fracking companies gave up on the idea. If, on the other hand, you conclude that the problem is solely to do with Britain’s post-Brexit energy trading arrangements with the European Union, you are going to waste a lot of time and effort negotiating a deal which will marginally alter your share of a fast-declining supply of gas which is already impacting the entire continent. And by the way, there is no law of nature which says that Russia must give Europe preferential treatment when it comes to its remaining – and dwindling – surplus gas.

There are many causes of the current – early stages – of the energy crisis. Some date back to gas and electricity privatisation. Some result from the failure to accurately assess the North Sea reserves. Others date back to New Labour’s decision to accelerate and over-extend Britain’s deployment of intermittent wind turbines and solar panels before anyone had figured out a scalable, cost-effective means of storage. Many of the company failures result from the Cameron-Osborne decision to allow the creation of new supply companies which lacked any gas reserves to insulate them from fluctuations in the wholesale market. And in practice, we will be better off when these fly-by-night operations have closed and we can better assess the true state of our energy supply industry. Nevertheless, the most important underlying problem is that gas – as with coal and oil – is a finite resource which we have extracted on a low-hanging fruit first basis. Having burned our way through the cheap stuff, we are obliged to move on to the difficult and expensive deposits. And like it or not, that means we will have to pay far more for energy in future than we have become accustomed to.

The bottom line here is that many of the things you are currently grizzling about – like lorry delivery shortages and rising prices of everything from food to microprocessors – are going to be a fact of life in the near future. Indeed, get this wrong and we face serious disruption as a consequence of random power outages crippling an economy which has been allowed to become increasingly dependent upon electronics to function. Whichever way you cut it, falling surplus energy (the amount left over after we have generated or produced energy) means falling discretionary economic activity. Rather like during the pandemic lockdowns, anything not considered essential will eventually not be done.

The next stage of this journey is bound to be a turn to nuclear power. This is because no politician – irrespective of statements to the contrary – is going to voluntarily preside over an energetic collapse of the economy. Indeed, it was only a matter of hours after the hike in gas prices and the beginning of the petrol shortage, before Rolls Royce had taken to the airwaves to promote their small modular reactors. In fact, the UK government had already given these – and six other over-the-horizon nuclear reactors – the green light three years ago. Of these, Moltex’s molten salt reactor is the only other design which look set to become commercially viable – with orders from Canada and Estonia as well as the UK. Crucially, unlike fossil fuels, there is more than enough uranium (and thorium if anyone can commercially breed uranium from it) to potentially power and grow the global economy. The high cost of nuclear is the result of the build and safety cost of large, pressurised water reactors rather than the fuel.

The issue at this stage is not so much whether new – fourth generation – nuclear can be developed, as whether it can be developed at the scale and in the time required. Europe faces an energy gap through the mid-2020s. But even the smallest new reactors are going to take a decade to deploy. And even then, they are no substitute for the diesel oil which currently powers the global economy.

In the meantime, there are three key steps that we can take to at least mitigate the crisis which is now unfolding. The first is to incorporate the current gas and electricity companies into a single national body so that the quasi-market cannot be used to hide the true costs of electricity generation. This may involve full nationalisation or something akin to what is being done with Britain’s railways. Either way, the primary aim of a new national energy industry must be to provide firm – 24/7 – electricity. Price concerns should be relegated to third place behind ensuring security of supply; with energy poverty being resolved through the social security system rather than faux competition between companies.

Second, we desperately need to be realistic about the cost of everything in an energy-constrained economy. Allowing multinational corporations to offshore large swathes of our manufacturing for the sole purpose of extracting greater profit has left us dangerously exposed to the breakdown of supply chains which will happen frequently as surplus energy declines. In many cases, we will either do things locally or regionally or they won’t get done at all… and we will all need to get used to it even if it means giving up things that we have come to expect.

Third, we need to urgently drop the techno-utopian fantasies promoted by charlatans like Elon Musk and by misguided technocrats like Herr Schwab. These are as much quack remedies as getting a better deal with the EU to secure access to gas which is no longer there or hydraulically fracking shale deposits from which most of the gas leaked hundreds of thousands of years ago. If a technology doesn’t exist – at least as a demonstration prototype – then we are out of time to develop it. And if it exists as a mature technology – like a wind turbine or a battery – then all of the viable improvements have already been made; if it isn’t up to the job today, it never will be.

We may rue the long chain of political and economic decisions taken between the first energy shock in 1973 and the onset of energy depletion in the 2020s. But casting blame gets us nowhere – and in reality, all of us have participated in and endorsed at least some of the decisions which have brought us to where we now are. What is required at this point is neither recrimination nor speculative fantasy. Rather, we need clear thinking about how we manage an irreversible period of economic shrinkage – something no living human being has had to contemplate. We have two options: Manage the process to avoid the worst of the negative consequences; or attempt to maintain business as usual and face a major collapse of both the financial and the real economy. We may hope that clever people somewhere else will figure out how to generate future surplus energy… but we would be fools to rely on it.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.