Related Articles

|

|

The recent, spectacular increase in the price of gas has created a sense of crisis not seen outside the financial sector since the early 1980s. In Europe in general and the UK in particular, it has begun to expose the folly of having an economy entirely dependent upon imports; including imports of the energy that powers everything we do. The conceit, of course, was that because we have gone much further than anyone else in deploying non-renewable renewable energy-harvesting technologies (NRREHTs) we were somehow less dependent on fossil fuels when events this week show that we are, in fact, more dependent than ever.

The deeper crisis though, is economic because without growing energy we cannot have a growing economy. This is obscured to some extent by GDP figures which count the movement of bits in bank computers as real economic growth when in reality, they merely add a new mountain of unrepayable debt to an already massive mountain of unrepayable debt. In the real world where the rest of us live, nothing gets done unless there is sufficient surplus energy to power it.

Setting aside for a moment the environmental imperative to cease polluting the planet, if it were possible to stabilise our fossil fuel consumption at 2019 levels, then we have some 50 years’ worth of accessible (proven reserves) of oil; 53 years of gas; and 115 years of coal. But flatlining is something that only happens in recessions. In the economy that we have come to take for granted, year-on-year growth in energy consumption is the precondition for improvements in prosperity:

This suggests that we have far less than 50 years before we run out of oil and gas if we insist on continuing to grow the rate at which we consume it. We should also note here that while fossil fuels are technically interchangeable to some extent – coal can be used to make synthetic oil and gas can be used to power some light vehicles – the costs to the economy would be eye-wateringly high. And so our additional years of theoretical coal consumption are not going to save us.

There are though, two additional show-stoppers here. The first is seen most clearly in Europe’s current problems. The first to industrialise, the European states were also the first to burn through their fossil fuel (and mineral) reserves in order to create the high standard of living enjoyed today. But that standard of living now depends upon the oil and gas-rich states of the former Soviet Union and the Middle East and North Africa not aspiring to a similar standard of living; so that their fossil fuels are available for our consumption. The world, of course, does not work that way. And these states are consuming increasing volumes of the oil and gas they produce to raise their domestic standards of living:

It is no longer enough for global production to grow at the current – or at least pre-pandemic – rate. To compensate for the oil and gas lost to producing states’ domestic economies, European states require a big increase in the rate of production. Which brings us to the second show-stopper: we have extracted fossil fuels on a low-hanging-fruit basis. That is, we began by extracting the cheapest and easiest deposits first before working our way toward the difficult and expensive ones. This is one reason why global oil production peaked in 2018 – there is still plenty of oil beneath the ground, but we can only afford to produce a fraction of it.

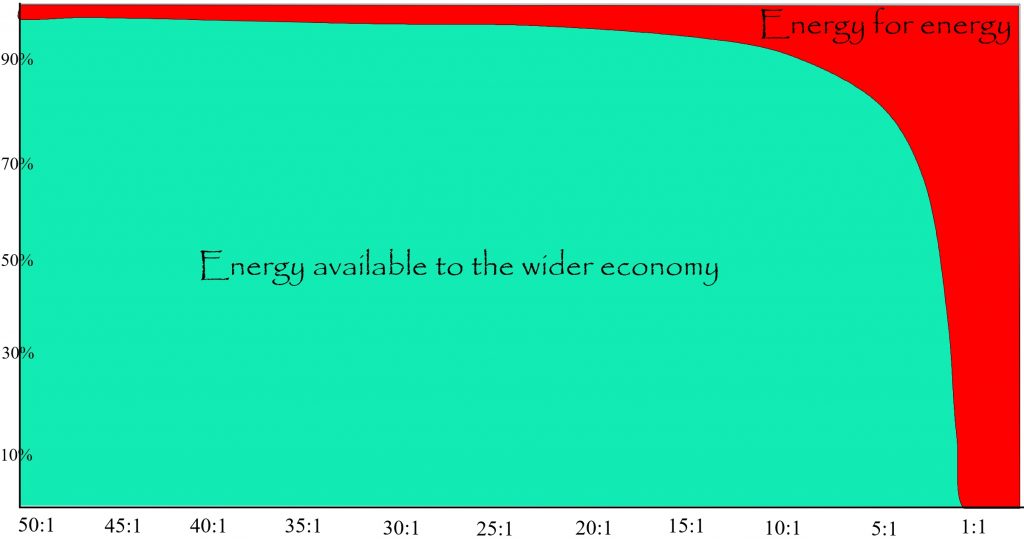

This is not simply a matter of money. Indeed, as we saw with fracking in the aftermath of the 2008 crash, financial engineering can temporarily allow companies to produce oil and gas which is almost entirely unprofitable. But the real phenomenon underlying this financial chicanery concerns the energy cost of energy – the amount of energy required to produce a unit of energy. In the case of fracking in the USA, for an input of the energy equivalent of one barrel of oil it was possible to produce five barrels – far less than the 20:1 minimum ratio required to operate an advanced industrial economy. It is this which is the true silent killer behind our growing energy woes because the energy sector of the economy is tiny in comparison to the non-energy sectors:

As the energy cost of energy increases, so the amount of the total energy which has to be diverted to energy production forces a sharp decline in the non-energy sectors of the economy. Different economies experience this situation in their own way. For over-developed states like those in Western Europe and North America, the consequence has been economic stagnation which has only temporarily been mitigated by massive volumes of central bank stimulus and ever lower interest rates – the aim no longer being to repay debt, but merely to hold down the cost of servicing it. In the developing states where living standards, labour costs and government regulation is far lower, it has been possible to maintain modest growth in the decade following the 2008 crash. However, even before the pandemic, those states were beginning to experience economic stagnation too.

The question which follows from this, is how rapid will the decline be? The answer, unfortunately, is that without careful harvesting and management of the remaining energy, we will likely plunge over the edge of a looming net energy cliff:

While we may have a theoretical 50 years or so of oil and gas available to us then, there is good reason to believe that in reality we will be lucky to have even half of this. Indeed, with oil production already falling, and given that producing gas relies heavily on oil-powered machinery, we may be lucky if we have more than a decade of gas available to us.

Does this mean that 2021 gas production will be humanity’s gas peak – the high point of our endeavours? It might be. Although Mr Putin’s use of gas shortages to cajole the EU Commission into finalising the Nord Stream 2 pipeline has echoes of the 1973 OPEC oil embargo. Not that we should take comfort from this. It was precisely the peak of the cheap USA oil deposits which created the shortages which allowed OPEC to assert itself. In the same way, it is European shortages and high prices which enable Putin to dictate future terms. Which means that, perhaps, with a mild winter and some additional investment as a result of the current high prices, it could be a year or two yet before we can say categorically that we have passed the peak of gas production.

In a sense though, the exact date of the production peak doesn’t really matter. Because what we are currently experiencing is an absolute energy cost limit asserting itself. While the current establishment media are exercised with the short-term inflationary impact of higher prices, the true crisis – which is readily visible in our city centres – is in discretionary economic activity.

This is the money manifestation of the rising energy cost of energy. As the price of energy increases, so too does the price of everything in the economy which requires energy to produce. To some extent, producers and retailers will absorb the rising cost – for example, by cutting “wastage” in their own operations. But ultimately, as with Kraft Heinz this week, they will tell consumers that they are going to have to get used to higher prices. In reality though, companies like Kraft Heinz are going to have to get used to falling sales. Because any product which is not essential is going to struggle to remain profitable as the energy cost of doing everything increases.

One reason why the UK is an extreme outlier in this crisis is due to the huge levels of inequality. While government departments and business executives make decisions based on averages – such as the official rate of inflation or the average wage – this data is now dangerously unrepresentative of real rates of prosperity. In the UK, the median household income – the half-way point on the income ladder – is some £6,000 lower than an average which is distorted by a small number of extremely high earners at the top:

This can, for example, lead governments into wrongly believing that the economy can withstand increased taxes and cuts in spending; businesses into believing that there is room for price increases; central banks into believing there is scope for cutting stimulus and/or raising interest rates; and investors into believing that high prices will translate into high returns.

The problem is compounded by an official rate of inflation which under-reports the vast increase in the cost of essentials like housing, electricity and gas, food and transport, while over-reporting the falling cost of discretionary items like electronic goods, trips to the cinema, dining out and – at least pre-pandemic – holidays abroad. For the growing precariat at the bottom, the current rise in fossil fuel prices has led to the unenviable choice between food and heat this winter. But even for those in a more comfortable financial situation, the increased cost of essentials means a switch in spending away from discretionary items. And since the discretionary sectors of the economy are far larger than the essential ones, this points to stagflation as businesses producing and/or selling discretionary items go out of business even as the price of essentials climbs ever higher.

This is the neoliberal “free market” version of peak oil and gas, but it will be distorted by governments which are largely clueless about energy-based economics, being driven to intervene in the face of public pressure. In the UK, for example, the government has already given a temporary subsidy to keep up the production of carbon dioxide, and is under pressure to support high-energy consuming industries like steel and ceramics. Moreover, the hit to household living standards has already raised questions about the “green” subsidies currently added to household energy bills. Ironically, while the current opposition (in name only) has ruled out nationalisations, it may be that the Tories will be obliged to do so in the event that critical industries begin to fail.

Either way, so long as the political choices before us remain focussed on economic growth, then they will fail simply because we have reached the point where non-financialised growth is no longer possible. The only real question before us – irrespective of whether peak gas is today or five years from now – is whether we are prepared to harvest and manage the energy that remains available to us so that we might save at least some of the benefits of an advanced civilisation, or whether we are going to waste it on such frivolities as flying private jets to conferences on climate change or launching billionaires and their cars into space.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.