Related Articles

|

|

The Indian government ruffled a few feathers at the COP this morning, by raising the thorny question of the £722bn they were supposed to receive to aid their transition away from fossil fuels. Because, when all is said and done, the proposed transition is all about money. Decommissioning the old fossil fuel infrastructure will not happen unless states and private investors stump up sufficient cash to pay for the materials, equipment and workforce required to do the job. And at the same time, an entirely different group of workers, materials and equipment will have to be funded to build out the new, bright green infrastructure.

To aid things along, states will also use legislation to force the hands of businesses and households. The current UK government’s decision to legislate a ban on new internal combustion engine cars from 2030, for example, has forced the car industry to switch investment toward EVs. The ban on coal power plants from 2025 may provide the more realistic example, however, because of its unforeseen consequences – such as companies closing power stations early to save on maintenance, and the threat to energy security which has now emerged. Nevertheless, it is some combination of legislation and money which will drive the process.

The same can be said, of course, for any campaigning/political issue. You can count on one hand the number of campaigns which have called for less state spending and the revoking of laws. Most often, new law and additional spending underpins demand for reform, while failing to spend and/or legislate is among the biggest sins a government can make.

So far so good. Except that both laws and money are merely ink on paper. They do not, in and of themselves change anything. Imagine, for a moment, you are the proverbial shipwreck survivor on your desert island. Lacking sufficient food and drinking water, your days are numbered. But then a passing aeroplane appears to offer salvation in the form of an emergency package parachuted down to you. You tear into the package, saliva dripping from the side of your mouth as you imagine the tinned food inside. But to your horror, you discover that the package contains a copy of a new law banning hunger on desert islands, together with a pile of banknotes that you might use to purchase some drinking water. Laws and money, then, are only useful insofar as they can redirect available resources – in this case, food and water – but are entirely useless when resources are not available.

This is obvious at a small scale – like a single person on a desert island – but is often obscured by the complexity of developed civilisations where resources are nominally available. Even in relatively primitive civilisations by modern standards, complexity served to obscure the resource implications of political decisions. As I explain in my book, The Consciousness of Sheep:

“Complexity, when it does occur, is always a response to the unforeseen consequences of prior solutions. Introducing coins as a means of paying soldiers and merchants, for example, makes theft and counterfeiting of money possible. This means part of societies’ surplus had to be invested in protecting the money supply. In a simple society, this might just mean allocating some soldiers to protect the coins when they are distributed, and to stand guard on market days. But even this apparently simple solution comes at a cost:

- The soldiers have to be fed and clothed

- Peasants – somewhere – have to produce this additional food

- A weaver will have to produce the additional clothing

- Blacksmiths have to do additional work to provide them with arms

- Additional resources and energy have to be found to allow blacksmiths to create the arms

- And, of course, someone else will have to be drafted into the army to take over the duties the soldiers had been performing.

The exact ramifications of this process would be neither known nor knowable to those making the decision. They will merely have been aware that people stealing money were eating into their surplus. And since the way to protect against robbery was to allocate guards, that is what they would choose to do. They would most likely not even think about the additional work for the farmer, weaver and blacksmith; still less the supply of resources and energy that would be required. They would, if you will, push their complex civilisation slightly out of balance, and leave it to individuals within it to try to find a new equilibrium.”

The only differences today are that there is far more complexity and the potential for negative unforeseen consequences is exponentially greater. Consider, for example, the current haulage crisis. It is not simply a shortage of lorry drivers – in fact, the UK has more than enough qualified HGV drivers. Rather, if is due to the confluence of unforeseen consequences from a raft of policies of both states and private companies, including:

- Legislation making drivers personally responsible for everything from vehicle safety to transporting illegal migrants

- Legislation changing the tax status of self-employed drivers

- The centralisation of giant distribution hubs with long waiting times and poor facilities

- Local council by-laws that ban parking near to toilets, shower facilities and food outlets

- Pay and conditions that have been allowed to deteriorate to the point that almost any other job is better

- Brexit and the pandemic restrictions causing Eastern European drivers to leave and not return.

These are merely the direct causes. Less obviously, Blair’s push to get 50 percent of school leavers into higher education is now being felt, as fewer school leavers have been trained in non-academic work skills including HGV driving. In this respect, applying policy of any kind to a complex globalised economy looks a lot like hanging poor wallpaper – you push a bubble down here only to cause more bubbles to appear over there.

One saving feature of our complex, globalised economy remained true for the best part of three centuries. This was that whatever changes we made, there were sufficient resources available to allow the system to accommodate them and to return to some kind of equilibrium. What began with small pits to carve out minerals gradually morphed into literally moving mountains to expose the resources beneath. Politicians could pass laws and borrow new currency into existence, and the economy would provide all of the necessary resources to bring the desired policies to fruition.

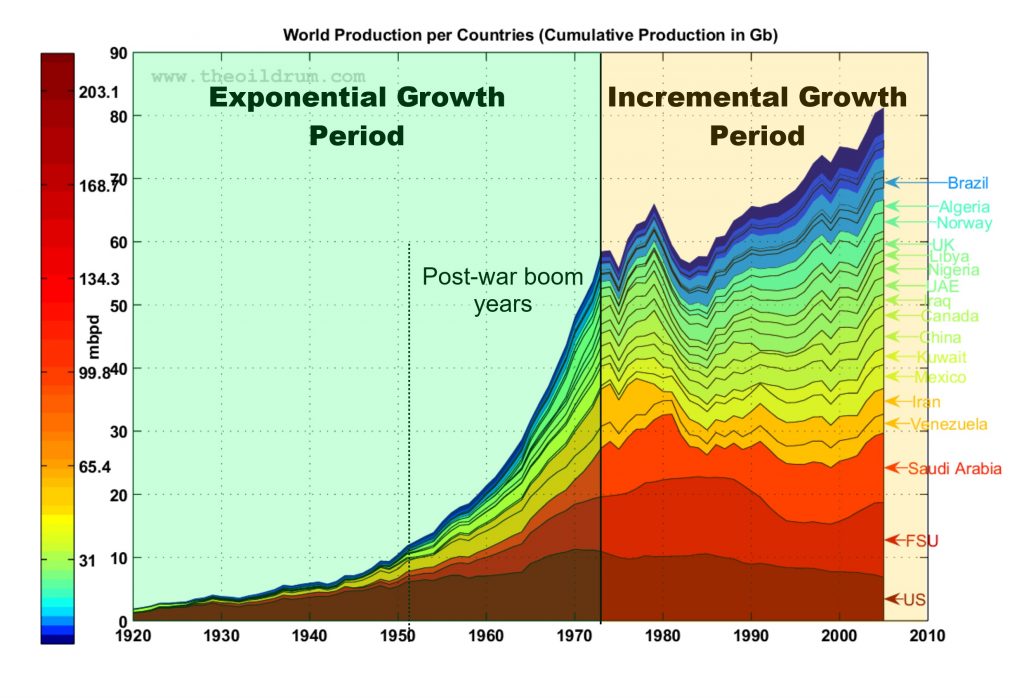

But something changed around the year 1970. Most notably, the US dollar – which had provided the financial foundation of the post-war economy – stopped working. Instead of facilitating economic growth, printing new dollars began to generate inflation. Why? Because – largely unseen by economists and politicians – exponential financial growth could no longer generate exponential resource growth. This was the result of a single process unfolding in both mineral resources and, crucially, in energy. In both cases, the industrial economy had operated on a “low-hanging-fruit” basis – using up all of the cheap and easy resources before moving onto more expensive and difficult ones. But so long as energy remained cheap and easy, so that energy consumption could grow exponentially, resource growth could also grow to meet whatever commercial or policy aims the combination of legislation and spending desired.

Most obviously, what changed in 1970 is that US land-based, conventional oil deposits passed their production peak. In the financial field, this brought an end to the Texas Railroad Commission’s monopoly over world oil prices. Less obviously, it marked the point at which global oil production ceased growing exponentially:

Real economic growth was still possible after 1970. But as the energy cost of delivering energy to the end user rose remorselessly, so the tendency for new legislation and new currency to translate into inflation rather than real growth increased accordingly. The post-war boom was confined to the history books, even though economists and politicians continued to treat it as the “normal” that humanity would eventually return to.

The opening up of new – albeit more expensive – oil deposits in Alaska, the North Sea and the Gulf of Mexico brought a degree of stabilisation from the mid-1980s; and should have been used to begin the transition to a less material economy. Instead, the politicians and economists used the new oil to underwrite the debt-based boom which came to grief in 2008, following the global peak of conventional oil production in 2005.

By the beginning of the century, the rising energy cost of energy – and the resulting increased cost of resources across the board – had rendered non-financial growth in the developed economies impossible. However, developing economies such as China and India, which used cheaper labour and operated to lower environmental and health and safety standards, continued to grow during the first two decades of the century. But this was already coming to an end before the Covid pandemic arrived to accelerate the processes of decline.

The problem we face today is similar to, but much worse than, the crisis of the 1970s. Then, there was a cultural overhang – which persists to some extent today – in which economists and politicians believed that the conditions of the post-war boom could be recreated through a combination of legislation and currency creation. Instead, of course, they first created inflation, then they created a depression, then they pumped up a debt-based bubble. What they didn’t do – and what we must surely accept they will never again do – is to recreate the boom conditions of the post-war years. Today the problem is made worse by the fact that energy production growth is at an end, even as the cost to the end user is rising out of control. And this puts us firmly in economic collapse territory:

In terms of the economy as a whole, this spells disaster because an increasing proportion of the dwindling energy available to us must be used to secure future energy. This means that we no longer have the energy – and hence the resources – to operate the totality of the globalised economy which we built on the back of the last spurt of fossil fuel production growth.

Translate that into the day-to-day experience of households and businesses – mediated and distorted to some extent by central bank policy and currency creation – and we find that an increasing proportion of income is having to be spent on essential items, while discretionary spending falls across the economy. Which is fine – for the moment at least – if you hold shares in an oil refinery, a gas power station or local food production. But heaven help you if you or your business is engaged in one of the much bigger discretionary sectors of the economy. Because if you thought the retail apocalypse of the last decade was a problem, you are going to be horrified by what comes next.

Not least, because governments and central bankers still hold onto the insane belief that they can steer us back to the once and done boom years 1953 to 1973. Consider the UK government’s claim that they are on the verge of creating a high-skilled, high-wage economy. This at a time when gas prices have risen by 400 percent, and petrol and diesel are at an all-time record high. These costs alone, are sufficient to throw the UK economy into a serious recession – possibly as early as next year. But on top of them, the government has directly introduced additional taxes and social security cuts, and is indirectly adding to the number of “green” levies added to household energy bills. Local councils are also waiting in the wings to hit households and businesses with big local tax hikes designed to claw back some of their pandemic losses. And to add to the misery – and wholly failing to understand that debt repayments are treated by most of us as essential – the central bank is planning to increase interest rates before businesses and households have had chance to respond to the other rising costs.

It is against this backdrop that we must now consider the auction of promises which is about to emerge from COP26. Because when governments talk about new legislation – such as the proposed ban on gas central heating – new taxes – such as a likely new carbon tax – or additional spending – such as on the proposed nuclear power plants at Sizewell and Wylfa – what they think they are proposing is the drawing forth of entirely new fossil fuel energy and mineral resources like we did in the aftermath of the war. Whereas, what they are really proposing is the wide-scale reallocation of current fossil fuel and resource production away from existing economic activities to their chosen projects.

This may sound fine if the proposed projects offered to replace the energy that it costs to deliver them. But none of the energy technologies currently on offer – still less the ones, like carbon capture and storage, which don’t exist – generates more energy to the end user than the fossil fuels they are supposed to replace. The problem being that we – largely unconsciously – use currency as a proxy for future energy, in the belief that there will be more energy tomorrow than there is today.

Everyone who took out a mortgage or a loan, every commercial bank whose business model is designed around debt-based “bank credit” – which makes up 97 percent of our “money” – and every government that borrowed by auctioning government bonds on the promise of future tax revenue, made the implicit assumption that the real economy will grow at a sufficient pace to repay the debt with interest. Indeed, one of the reasons why interest rates have fallen to medieval levels – and why productivity gains have all but disappeared – is that we no longer have the energy and resource growth to support the borrowing we have already engaged in.

Rising energy costs alone now threaten to unravel the global economy. Pull the rug out from what remains, via tax increases, interest rate hikes and the now inevitable rising cost of energy and everything in the economy which requires energy, and you have a recipe for a financial collapse on a scale that makes 2008 look like a cake walk.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.