Related Articles

|

|

One of the greatest skills of our political leaders is the ability to tell a blatant lie while keeping a straight face. Like the one about how inflation – officially running at 9.1% last month – is being fuelled by workers’ pay increases. That one has gathered pace this week as we face the first national rail strike in years. After more than a decade of falling median real wages, when the only people getting rich were the oligarchs, the corporate CEOs and their lackies in the technocracy, it is doubtful that wages are responsible for even a fraction of a percent of the increase in prices. Nevertheless, someone has to be demonised… someone must be blamed.

Dig beneath the headlines, and a somewhat different picture is already emerging. Demand destruction is already happening. Just four items are holding average prices up – household energy (electricity and gas) transport (oil) second hand cars (chips) and food (fertilisers). Strip these out of the figures and you get an inflation rate below one percent – very much in line with where it was prior to the lockdowns. More importantly, it shows us that the price increases battering the UK economy are the result of factors beyond these shores and which our government and central bank are powerless to resolve. As Thomas Fazi explains:

“The problem with all this is that — again, just like in the Seventies — the recent inflation has relatively little to do with excess demand and excessive wage growth. In fact, it has mostly supply-side origins, triggered by the Covid crisis and now the Ukraine war, and rooted in the systemic deficiencies of neoliberal globalisation. From a Western perspective, the global lockdowns of 2020 and 2021 caused a collapse of global supply chains in durable goods and industrial components, as well as of cheap, flexible and abundant labour in low and middle-income countries. These foreign supply-side bottlenecks, which in turn were exacerbated in several countries by domestic supply-side bottlenecks — such as a shortage of long-haul truck drivers and dock workers in the US and UK — are the reason prices were on the rise well before the outbreak of the conflict in Ukraine.

“In other words, lockdowns are to blame — not the fiscal measures adopted to dampen their effects. This is what we might call lockdown inflation, which is now flaring up once again due to the recent Chinese lockdowns.”

Fazi argues that the current clamour for higher interest rates is not intended to fend off inflation, but rather to create a depression in order to drive up unemployment:

“I would posit that once again, as in the Seventies, they are intent on exploiting the current inflation to engineer a recession and drive up unemployment in order to pre-empt a potential rise in labour bargaining power. After all, even if organised labour is still very weak, it is also true that labour markets — particularly in countries such as the US and UK — have been growing increasingly tight as a result of the post-lockdown surge in labour demand and Brexit in the UK. They are bound to remain relatively tight even in the future as the global economy undergoes a structural process of de-globalisation and reshoring.”

However, even the central bankers have expressed concern about overdoing interest rate rises. The latest Monetary Policy Committee meeting, for example, was split over a further interest rate rise despite rates being far lower than the economics textbooks (which are invariably wrong) suggest they ought to be. The problem being that nobody is entirely sure how exposed the banking and financial system is to the shock of its first recession since being put on life-support after 2008. Another deflationary debt default on that scale could well bring the house down. And following the rise of nationalist populism as a consequence of the last crisis, it is going to be difficult to bail out the system a second time.

Government is equally conflicted. The reason interest rate policy was handed to central banks in the first place was to take the decision out of the hands of politicians – a classic neoliberal device, allowing politicians to duck responsibility for monetary policy. But having done this, it makes little sense for government to stymie central bank efforts to slow the economy by handing out grants (money printing) to mitigate rises in prices. If the aim is to engineer a recession, then government should be raising taxes and cutting public spending. Except, of course, that government is also divided between those who believe that it is possible to engineer an economic soft landing and those who fear a deflationary debt default of epic proportions.

It is important to understand that the reason our Chancellor is handing out £650 to all of the low-income households in the country is not due to some damascene conversion, but because it is a politically adroit means of bailing out energy supply companies that would otherwise have failed this year. The same is true, of course, of all of those furlough payments that were made during the lockdowns, which indirectly supported the corporations by maintaining their cashflow from consumers. In purely economic terms, government could have achieved the same result by handing the cash directly to the corporations. But politically, that approach would have ended with guillotines on Parliament Green.

So what is to be done?

A good starting point would be to slay – or at least de-construct – the Volcker myth. According to the myth – although this is disproved in the records from the period – Paul Volcker chose to implement a massive rise in interest rates in order to create the recession which finally squeezed inflation out of the system. The reality though, is that the Iranian Ayatollahs had already done that – like today, causing oil prices to rise to a point that widespread demand destruction was inevitable. Indeed, Volcker and his colleagues were not even sure that raising the overnight borrowing rate – the amount the Fed charges commercial banks for borrowing central bank reserves – would even have an effect on the wider money supply… still less what that effect might be.

In practice, we know to our cost exactly what the effect was. Just at the point when the economies of the USA, the UK, and Europe needed productive investment in modernising their manufacturing base, ultra-high interest rates had two key impacts. First, they drove the value of the currency far higher than the real economy could support. The result was that domestic manufacturing couldn’t compete in world markets, causing a cull of domestic production and beginning the neoliberal process of offshoring. The second was that the relative positions of the productive and banking sectors were reversed. Instead of being a relatively small service to a much bigger productive economy, banking and finance metastasised to dominate the economy, creating a rentier economy which has little beyond money printing and money laundering to offer to the wider world in exchange for those imports – fossil fuels, food, computer chips, etc. – which are now in such short supply.

Although not directly responsible, we might also lay at Volcker’s doorstep indirect responsibility for creating the conditions for the Big Bang deregulation in 1986, which among other things took the brakes of the banks’ ability to create unlimited currency out of thin air. Prior to the Big Bang – more so in the UK than the US – a large part of the money supply still came in the form of notes and coins. But with the onset of computerised banking, the amount of currency the banks could create in the form of loans seemed almost limitless. Until, that is, it reached its limits in 2008 – in large part because the system had run out of people to lend to.

Post-2008, the problem has been that the excessive debt never went away. Quantitative easing put a floor beneath the banking system while low interest rates kept the debt manageable. But the absence of economic growth and the slow but remorseless decline in the real economy left the system balancing precariously on a tightrope, with the threat of inflation on one side and a deflationary collapse on the other. Which is why our leaders needed to avoid at all costs anything so foolish as locking down the economy and crashing the global just-in-time supply chains or having an undeclared economic war with the Eurasian resource regions of the world.

It is essential that we understand that for the UK at least, rising prices are due to international issues and not because of loose domestic monetary policy. As a result, no amount of interest rate rises or government austerity programmes are going to bring prices down. Only demand destruction and/or expanded supply can do that. And insofar as monetary policy has played a role, it is the Biden administration’s decision to open the currency spigots and spew trillions of new dollars into a barely recovering post-lockdown global economy that has exacerbated supply shortages. By pulling commodities that were already in short supply into the US, it was Biden, not Putin, who helped drive up world prices.

For the moment, the Brent oil price has settled around $110 to $120 per barrel – slightly above the limit that the economy can withstand without tipping into a depression:

This is likely why, despite ongoing shortages and predictions of $200 oil, producers seem unable to drive prices higher. Nevertheless, the current situation is unsustainable. And there are only two means of resolving it. The first and least likely is that we suddenly discover a giant reserve of cheap and easy oil which we had somehow overlooked until now, and which might be brought on stream rapidly. In the absence of such a ready reserve, the more likely outcome is that the economy will have to adapt to the new situation and reduce demand accordingly.

We are already witnessing this to some extent already. Directly, people are saving on fuel by cutting down on non-essential journeys. One reason why the rail companies have provoked the current strike is that they stand to save millions of pounds in fuel costs and wages. The same goes for airlines cutting thousands of flights. And indirectly, we are witnessing nationwide belt-tightening as people’s spending shifts away from non-discretionary items in order to manage the rising cost of essentials.

The problem in the current moment, is that it takes time for these changes to filter through the economy. For example, demand for household goods was still increasing in May. But this is likely because households have been attempting to replace items before the prices increase even further. In the same way, people booked summer holidays back in January – when prices were lower – and are likely indulging in some additional spending in restaurants during the break – preventing prices in this sector from going negative… although it is only a matter of time. Moreover, even after demand falls, businesses tend to try to hang onto their workers – for small business owners, it is hard to look a colleague in the eye and tell them they don’t have a job anymore. And even giant corporations are concerned about the loss of trained and skilled people. In short, even if demand collapses over the summer, it might be the autumn before we start seeing widespread unemployment.

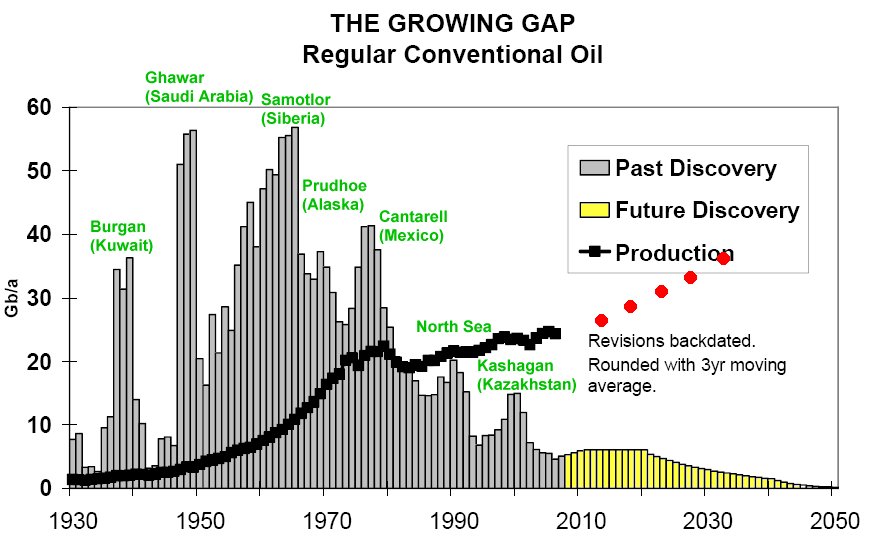

The broader question is whether oil prices can be brought down to a point where at least some economic growth can be achieved – as happened between 2015 and 2017 – or whether demand-destroying oil prices are a permanent feature of the future economy. There is good reason to think not, simply because oil production had already peaked in 2018. And while production has risen in the last year, it is still some four million barrels a day short of its pre-pandemic level.

While there are undoubtedly people within government who understand the issues around energy and resource depletion, it is doubtful that they have the ears of treasury ministers or central bankers. Not least because while the problem is simple enough to define, nobody has come up with a credible solution which doesn’t involve dramatically shrinking the economy. And so, ministers and central bankers are more likely to turn to economic textbooks that even they know should have been shredded in 2008. But what else can they do?

They face three broad choices. First, they can follow the Volcker myth and lean into a depression which is already happening as a result of rising energy prices and disrupted supply chains. Second, they can attempt to mitigate the impact of these price increases by printing and allocating more currency to those on low incomes. Third, they can do nothing in the hope that oil and commodity shortages alone will be sufficient to generate a soft recession without bringing the house down. The problem with the first approach – which is why interest rate rises have been small – is that the western economies – still reeling from the 2008 crash – are so fragile after the lockdowns that a depression could bring the entire system down. But allowing prices to rise unchecked while attempting to maintain demand, at least for those on low incomes, risks capital flight as domestic inflation eats into returns. The third option – doing nothing – might prove to be the worst of all insofar as it results in demand destruction and investment flight, generating a stagflation in which prices are rising even though businesses are going broke, and unemployment is rising. In the short-term, none of the options on offer is favourable to a government which would quite like to win the next election.

Perhaps the more important question though, is which option is best for the long-term. Here, much depends upon our understanding of the situation and our vision of our future. Many within government and the central bank will opt for the “creative destruction” view of economic development. This holds that ultimately, recessions and depressions are good because they clear the way for leaner, more effective businesses to emerge. The analogy of a forest is often used, with the idea that the giant, dying trees and cloying underbrush – the equivalent of zombie businesses and rent-seeking multinational corporations – block the sunlight (investment capital) from reaching the new saplings (entrepreneurial businesses) on the forest floor. By euthanising the dead wood, the story goes, we clear the way for a new round of economic growth…

But is this true?

The three big waves of economic growth in the three centuries of industrialisation have resulted not from deliberately engineered destruction, but from new and more powerful energy sources being harnessed for production. The first – at the dawn of the industrial revolution – was the efficient harnessing of renewable energy, and specifically the use of metal waterwheels to harness the volume of water required to drive industrial-scale cotton mills. The second – from around 1800 – was the development and deployment of efficient steam engines to harness the heat provided by coal. The third – from the late nineteenth century – came with the development and growing use of the internal combustion engine. At each stage, the increased energy available to the economy allowed for a big increase in economic growth compared to what had been possible previously.

Productivity – that other economic chimera which will be appealed to in ever louder tones in the coming months – is secondary to the energy source itself. Investment in technological improvements has, indeed, boosted economic growth down the ages. But we fall into the trap of mistaking the technology for the additional energy it delivers. What is actually happening, and over a longer timescale, is that the first, rudimentary technologies used to harness any new energy source are invariably inefficient – far more of the energy is lost as waste heat than is made available for productive work. Simple competition encourages a series of relatively cheap and easy improvements to the basic technology to greatly increase the amount of energy available for productive work, while decreasing the amount of lost heat. These are amplified by economies of scale and standardisation. But there is a thermodynamic limit. The more a technology is improved, the closer it gets to the point where no further heat loss can be prevented. But before this theoretical limit can be reached, technologies hit an economic barrier, where the cost of the improvement is greater than the returns available to the economy. The two famous examples I often use are the Wright Flyer and the Concorde, and Trevithick’s 1804 steam locomotive and Gresley’s Mallard. In both cases, the essential technology is the same – an aeroplane and a steam locomotive – but the first is ripe for a raft of cheap and easy improvements, while the second is a technology which has overshot its economic limit – both Mallard and Concorde were playthings of the wealthy which had to be subsidised from the taxes levied on ordinary people… which, when all else is said and done, is why nobody has made a serious effort to better them.

The problem facing us today is that our oil age technologies are hitting these same economic limits:

Throughout three centuries of industrialisation, the way in which we have overcome this limit on productivity gains is to switch to a cheaper and more powerful energy source:

This presents us with a serious problem today, because the only alternative energy sources available to us today are less powerful, less versatile and more expensive than oil, whose technological limits were are already reaching. In other words, there are few, if any, technological – “productivity” – improvements which can be made to increase economic output and there is no means of boosting the absolute energy available to the economy. Indeed, because we extracted the cheap and easy fossil fuels first, an increasing amount of the energy which remains has to be consumed in producing energy itself, so that the surplus energy available to the wider economy is falling.

There are no entrepreneurial saplings waiting for the deadwood to be cleared to propel us into a new golden age of economic growth. And any attempt at “creative destruction” risks undermining key critical infrastructure in order to maintain financial interests which are going to be of little – if any – use in the process of de-growth that we now face. If we had true leaders – rather than the basket of sociopaths, spivs, clowns and gentlemen whose proper place is in a care home for dementia – we would be actively planning and discussing what kind of economy is possible within the limits of the energy and resources available to us, and how we might get there without starving or otherwise euthanising perhaps two-thirds of the current population. Instead, the only “plan” on the table is Herr Schwab’s Great Green New Reset which, absent some yet-to-be-discovered high-density energy source, breaks so many of the laws of physics that only a lunatic or an economist would believe it possible.

Unfortunately, a large number of the sociopaths who do think it is possible to defy gravity are in charge of central bank monetary policy and government energy policy. And so, rather than a clear understanding of our predicament together with policy decisions designed to mitigate the gathering storm, we can look forward to outdated economic theories and magic thinking combining to produce the worst of all worlds – one where mass starvation and hypothermia are all too likely. And worse of all, they will fail in their own terms. Because both the debt mountain and the supposed wealth based upon it are entirely dependent upon continued real economic growth which is now impossible.

Of course, real wealth can outlive an economic crash. A factory, a power station or a railway still exists after the company which owns it goes bust. The question is whether neoliberal governments can be persuaded to intervene to recapitalise them before someone else turns them into scrap. But this requires a degree of intervention that conservatives tend to reject and a type of intervention that socialists tend to oppose. Because the issue at hand is about determining which infrastructure is critical and which we can allow to fail. And this, in turn, requires a degree of hard-headedness that few politicians are capable of deploying. Instead, in the short-term we can look forward to the rapid push to introduce central bank digital currencies so that they can turn interest rates negative once it becomes obvious that we face the biggest slump in living memory.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.

{kind=link}