Related Articles

|

|

What, then, are we to make of the Bank of England following the US Federal Reserve in raising interest rates by 0.5 percent? If Bank of England Governor, Andrew Bailey is to be believed – and there is good reason not to believe him, the central bank is merely following the discredited theory that the only way to bring price rises under control is to make borrowing more expensive. According to Dearbail Jordan & Michael Race at the BBC, the central bank has done this despite knowing that it will plunge Britain into a recession for more than a year:

“The Bank of England has warned the UK will fall into recession as it raised interest rates by the most in 27 years. The economy is forecast to shrink in the last three months of this year and keep shrinking until the end of 2023…

“Governor Andrew Bailey said he knew the cost-of-living squeeze was difficult but if it didn’t raise interest rates it would get ‘even worse.’”

The problem with this narrative is that Bailey knows full well – and if he doesn’t he should be fired from his £500,000 position immediately – that there is no inflation – in its true meaning – in the UK economy. Prices are not rising because of the temporary and now gone additional currency during the two years of lockdown, but because of supply shortages and broken supply chains which cannot be fixed – and will likely be made worse – by reducing the currency supply – some 97 percent of which is borrowed into existence.

It is likely that Bailey is aware that Britain’s domestic economy – once energy imports and supply chain issues have been stripped out – is already in recession, and that further increases in energy and food prices in October and January point not to a mere “recession” but to a cascading collapse of the UK economy. So that if, as Bailey claims, a recession is required to crush demand in the economy – via business closures and far higher unemployment – then further interest rate rises are unnecessary. They are the equivalent of throwing petrol on a fire that is already out of control.

However, as I implied earlier, Bailey is a liar. The reason the central bank has raised interest rates has little to do with the domestic economy, and clearly pays no attention to the detrimental impact on ordinary households. The truth that Bailey dares not give voice to, and that the political left refuses to hear is that Britain is on the verge of bankruptcy – it has total liabilities of more than £20 trillion on an annual GDP of just over £2 trillion… and nearly half of that outstanding debt is denominated in dollars.

This is where the political left gets the economy wrong and where Bailey is likely correct but misguided. According to the left, debt is not a problem because Britain is a sovereign country and can print as much currency as it needs to cover its debts. This is both true and banal. Sri Lanka is also a country which can print as many Rupees as it needs to pay its debts. But as we have seen recently, this comes at the high cost of not being able to afford the dollar and yuan denominated imports that it needs. One reason why Britain continues to experience price increases despite oil and commodity prices falling is that international traders have been moving out of the British pound and into the US dollar. And if this movement were to become a flood, it is doubtful that what remains of the British economy can withstand the sovereign debt crisis which would inevitably follow.

Catherine Mann, an external member of the Bank of England’s Monetary Policy Committee, gave the game away back in June, as Chris Giles at the Financial Times reported:

“One of the Bank of England’s more hawkish policymakers has warned that the UK faces further rises in inflation if the central bank fails to increase interest rates as rapidly as the US Federal Reserve, causing the value of the pound to slip…

“She thought that incomes were being hit, but spending might prove to be more resilient, further embedding inflation, particularly if the BoE was seen to be reluctant to tighten monetary policy.

“In what she called an ‘extremely stylised’ model, she noted that when the Fed typically raised interest rates by 1 percentage point, sterling would fall because the BoE would not follow suit and UK prices would rise another 0.5 per cent.”

It goes without saying that whereas a devaluation of the pound is most damaging to the wealthy, higher interest rates cause the greatest damage to the poor and the middle class. And so, as in 2008, what the Bank of England is really doing is throwing the people under the bus in an attempt to bail out their friends and colleagues in the banking and financial sector.

This time though, their efforts will likely be in vain. It is not just higher interest rates which are sucking dollars back to the USA. There is broad awareness that the combination of disrupted supply chains and energy shortages have already caused – but it will take a few more months to become evident in the data – a massive economic shock for the European (including the UK) economies. German industry is already in freefall, and what remains of Britain’s manufacturing sector will be following once higher energy and food prices filter through later this year. And since none of the international lenders who create Eurodollars out of thin air is in a hurry to be the next Lehman Brothers, they are already moving investment out of Britain and the EU and back to the relative safety of the USA.

By raising interest rates, the Bank of England can temporarily strengthen the pound against the dollar by offering greater returns to international investors. Notice though, that this also results in both the government and corporate borrowers having to convert more pounds into dollars in order to repay their dollar denominated debt. But as the domestic economy slows and perhaps 90 percent of UK consumers are obliged to switch falling incomes from discretionary to essential purchases, obtaining the domestic currency to convert to dollars becomes ever harder. And so, we enter a “dollar death spiral” as governments increase taxes and corporations increase prices in response to the consequences of rising interest rates.

Meanwhile, the neoliberal right has fallen for another false economic metaphor – that of cutting down the dead wood in order to allow the green shoots of recovery to take hold. This was hogwash when Thatcher espoused it in the 1980s, and it is even more deadly today. We do not have “zombie companies” getting in the way of more productive ones… we just have zombie companies. And higher interest rates and lower government spending will serve only to crush them faster than would otherwise be the case.

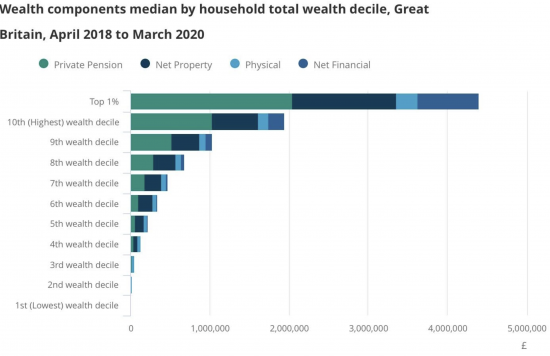

The truth about Britain – which we must acknowledge as a nation if we are to stand a chance of mitigating the worse of what is coming – is that we have been enjoying all of the benefits of the “curse of oil.” The North Sea allowed us to duck the structural economic reforms that were required in the early 1980s. Instead, we were able to borrow beyond our means using the income from oil and gas exports to underwrite a far higher standard of living than we could afford. And the fact that this was done in a grossly unequal manner – with ten to twenty percent of the population enjoying public and private largesse even as eighty percent of us experienced stagnation or falling incomes – makes repairing the damage all the harder today.

This, perhaps, is where Bailey may prove to be a fool as well as a liar. Because, as Richard Murphy argues:

“Now it just so happens that there is one group in society who do have too much money, as the BoE assumes right now. They, unsurprisingly, are the ‘haves’. Their savings can cushion them from the blows of price increases. They have money and other assets they can fall back on.

“Times are not hard for the ‘haves’ right now. And the BoE is just about to make it easier. They will actually have more to spend because of the BoE interest rate rise. No one else will.

“What this means is that counter-intuitively, the one group in society where there is a real need to reduce spending power because they are the one group who can push up prices in the way the BoE thinks happens are precisely the one group who will not be punished by BoE policy.

“But all those groups who do not have the spending power to increase prices are exactly the ones that the BoE is going to punish with its policy. They could not have got things more wrong if they tried.”

Murphy may well have a point here – although for reasons different to those he states. Attempting to stave off the coming sovereign debt crisis by raising interest rates is only a means of kicking the can down the road. The fact of the matter is that Britain’s manufacturing base was deliberately crushed and hollowed out by an over-valued pound which served the few at the expense of the many over decades since the 1980s. The correction – hard as it is bound to be – is more necessary today than ever before, precisely because a collapse in the value of the pound will make Britain’s exports cheaper even as it obliges us to start making those things that we currently import for ourselves or – in the case of discretionary goods – to forego them entirely.

Bailey will never raise rates to the point where they will cure rising energy costs and broken supply chains. Nor will he be able to maintain the pounds value against the dollar. What he could do, if only he was prepared to let his class take some of the pain for a change, is to allow the pound to fall closer to its true level. And if he won’t? Well, that makes him a liar and a fool because the people will inevitably answer his actions with the election of a populist government which will take the hard decisions instead.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.

{kind=link}