Related Articles

|

|

When economies fall apart, politicians point to issues of confidence. So it is, that this weekend we witnessed “Dagenham Liz” Truss blaming the collapse in the Pound on a “failure to prepare the ground,” rather than understanding it as evidence of the underlying weakness of the UK economy. This has echoes of George W. Bush in the face of the 2008 crash:

“If money isn’t loosened up, this sucker could go down…”

All it needed then, it seemed, was for Americans to get their credit cards out and get spending. And all it needs today, allegedly is for markets to get a grip and understand the growth potential of Truss’s trickle-down tax cuts.

This idea that economic crises are the result of a failure of confidence is seductive for politicians who know just enough about the economy to be dangerous while knowing far too little to act appropriately. Believing that the economy is financial in nature is likely the first error made by politicians and economists alike. From this starting point, it is all too easy to witness the panic on trading floors when the proverbial hits the fan, and to mistake this for some kind of psychological herd behaviour – like a herd of wildebeest fleeing an imaginary lion. In such circumstances, it falls to politicians and central bankers to inject an air of calm (along with some bailout cash) to get things working once more.

Except that – to stretch the metaphor – the herd is not panicking because of an imaginary lion; it is panicking because a pride of lions (stagflation) is closely following its heels even as a river full of hungry crocodiles (asset crash) lies before it. There were real world reasons for the run on the pound which followed (Kami)Kwasi Kwarteng’s ill-conceived mini-budget last Friday. The closest of these was the illiquidity of supposed “assets” held in the pensions industry and related concerns that the previous Monday’s Gilt (the equivalent of US Treasury Bonds) sale went badly, with investors demanding a much higher than expected interest rate for lending to the UK government.

The Bank of England’s return to quantitative easing appears to have taken the immediate steam out of the crisis, and Kwarteng’s U-turn on cutting the highest tax rate has helped calm political nerves, allowing the pound to return to its level immediately before the mini-budget. The underlying problems, however, remain unaddressed.

The problem lay not so much with tax cuts – which have previously, in some circumstances, boosted growth – but with the UK government’s inability to finance them… and, indeed, the hundreds of billions already spent on energy bailouts and lockdown support. The Truss claim that tax cuts will be self-funding because of the additional growth they will generate is though, economic illiteracy. Over the last decade, the UK economy has been borrowing £5 for every £1 of economic growth – and this gap is projected to get far worse over the coming decade because of the emerging crises in the underlying “real” economy. Indeed, even during the heyday of North Sea oil and gas revenues, governments struggled to engineer growth rates anywhere close to what would be required to meet the Truss proposals.

With Russian gas no longer deliverable – even if the EU and Russia wanted to reach a deal – because of the sabotage of the Nord Stream pipelines, European gas shortages are inevitable. The only question to be answered is how bad the shortages will be. And while Britain is not a direct importer of much gas from Russia, our energy supply companies still buy and sell gas on the European market. So that, if, say, German companies are prepared to pay more, they can bid the price up far higher than the UK government anticipates. In which case its borrowing to fund the energy price cap could easily spiral up into the hundreds of billions and, given market reluctance to buy Gilts, send interest rates well into double figures.

Even this though, only scratches the surface of the crisis, because politicians and economists fail to understand the true role of energy in the economy. Indeed, most economic models do not even regard energy as a separate category, seeing it instead as just another, relatively cheap, input barely worth mentioning. The reality – as you and I would quickly discover if we went without food – calories – for any length of time, is that energy is the starting point for everything within the economy. No food equals no workers. No fuel and no electricity equals no capital. As Steve Keen puts it:

“Capital without energy is a statue; labour without energy is a corpse!”

When the politicians talk about economic growth, what they are actually talking about is the creation of more of what physicists call exergy – the useful work which can be done with energy. Because of the inefficiency of machinery – and human bodies – a large amount of energy is simply not used, while more again is lost to waste heat. At best we might be able to convert 30 percent of the energy available to us into useful work (roughly the amount of sunlight a plant can photosynthesise). And so, there are but two ways in which we can have economic growth. The first is an absolute increase in the energy available to us at the beginning – 30 percent of 10,000 calories is a lot better than 30 percent of 1,000 calories. The second is through productivity – the process of minimising the amount of energy lost to inefficiency and waste heat.

The show-stoppers here are first, that there is no cheap and abundant replacement for the fossil fuels that are going away. And so, we have no means of adding to the amount of energy available to us. The second is that we have made all of the cheap and easy energy efficiency gains on our oil age technologies. Even in computing – the final frontier of the oil age – productivity gains are grinding to a halt as the limits of chips and memory are being reached. In short – and absent some yet to be discovered energy-dense alternative to fossil carbon – we cannot grow our exergy and so cannot grow the economy.

The problem is not just energy quantity either. In order to obtain energy, we must first expend energy. And if some forms of energy – such as, for example – obtaining shale gas from the UK’s twisted and fractured shale deposits – cost more energy to produce than they provide in return, they are simply not worth producing. It is here that things tend to go over the heads of UK politicians and economists, who believe that we can solve our ills via some combination of fracking, opening old coal fields, building nuclear power stations and erecting masses of wind turbines. These processes only solve the crisis if they are much cheaper than our remaining energy sources. And by “cheaper,” I do not mean only in price – although high prices do reflect the problem to some extent. Rather, it is the energy cost of proposed alternatives – the cost of building, fuelling and maintaining them which matters.

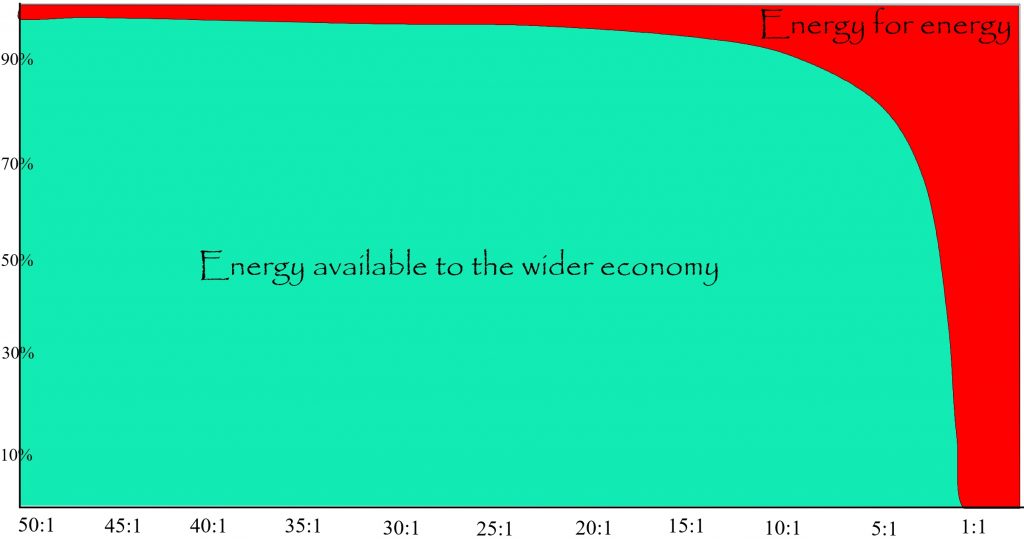

Put simply, at any time, an economy has a finite amount of energy with which to power all of its activities. This may increase – as it did when the UK opened up the North Sea – and it may decrease – as has happened in the UK since the North Sea peaked at the turn of the century. Until recently, a small proportion of this energy has had to be used to produce energy. The remainder has been available to power everything else:

Notice that, even on the eve of the current crisis, the proportion of energy consumed in producing energy – the “Energy Cost of Energy” – was but a small fraction of the economy, allowing for mass consumption of a host of discretionary goods and services beyond the day-to-day and month-to-month essentials like housing costs and food. This is one way of visualising the amount of surplus value that our various energy sources provide us with. Even at £100, for example, a single barrel of oil provides us with the equivalent of 4.5 years of human labour – which would cost us £110,700 at today’s average wage. That’s a more than 1,000 to 1 return on investment… little wonder, then, that the global economy goes into a tailspin every time oil prices become volatile.

The loss of value which accompanies a rising energy cost of energy comes with an additional sting in the tail. An advanced industrial economy requires a minimum to prevent it from collapsing. This results in a net energy cliff:

After three years spent destroying our global supply chains and sanctioning away the last of the world’s cheap energy, the economies of Europe – including the UK – are sliding over the energy cliff. As an illustration of this, as European energy has increased in cost – reflected in rising prices – heavy industry is already packing up and leaving for those parts of the world where they can still operate at a profit. As Irina Slav at OilPrice reported last month:

“Soaring energy costs in Europe are shutting down businesses and threatening a bloc-wide recession… more and more companies are switching into survival mode. That’s because, for a lot of them, the time is coming to renew their electricity supply contracts with utilities. Thanks to energy inflation, these are set to be much higher than the contracts for the current year, with front-year prices reaching over $1,000 in France and Germany…

“It looks like businesses packing and leaving for cheaper jurisdictions is yet another unintended consequence of the policies favored by European governments, especially in the energy department. It is also one more risk for the survival of the bloc as a competitive industrialized formation in the future…”

Ironically, among the industries to close or offshore production are the EU’s wind turbine producers – exposing the degree to which non-renewable renewable energy-harvesting technologies depend upon cheap and abundant fossil fuel energy in their manufacture. Most likely then, China will be the main beneficiary of any future attempt to solve the European energy predicament by building more windfarms.

The loss of heavy – and often critical – industry is merely the beginning of the slide over the net energy cliff. If governments allow critical industry to fail, then they will face a balance of payments/foreign exchange problem as they seek to replace lost domestic production with imports. Alternatively, they might remove energy (currency) from elsewhere in the economy to prop-up unprofitable but essential manufacturing. Either way, the result is the continuing withering of the wider economy. Lost manufacturing causes lost employment, which results in lost demand, which results in further losses… particularly in the manufacture and sale of non-essential items.

This is the real – though largely unseen – reason why both Truss and her critics are wrong, since both imagine that continuing growth is built in. After all, recessions and depressions aside, growth has been a core characteristic of a three-century long, fossil fuelled, industrial age. Like water to a fish, we simply take it for granted. The 110 billion cubic meters (bcm) per year of cheap gas lost from Nord Stream 1 alone, is enough to present Europe with a major energy crisis for several winters to come. And together with the loss of oil and coal imports from Russia and Kazakhstan, render much of the continent’s key export industry unprofitable overnight. In such circumstances, as Thomas Fazi – who also sees the crisis in financial terms – at UnHerd concludes, the UK would do better to face the new reality:

“In the end, the best option for the UK’s authorities might be to accept there’s little they can do, in the short term, to rein in inflation that is largely supply side-driven, stop attempting to prevent the pound from falling in the name of some misconceived ‘strong pound’ policy (which is what led to the government’s flawed response to the 1976 crisis) — and focus instead on protecting people and businesses through increased government spending.

“This may or may not be inflationary. But the alternative — giving in to market pressure to raise interest rates and rein in the deficit — is almost certainly bound to be worse.”

This, I believe, was Truss and Kwarteng’s real failure. Facing the biggest economic crisis in living memory, with businesses failing and households struggling to afford food and heating, and in the wake of the death of a widely loved and long-lived queen, the new government’s first policy announcement needed to be truly Churchillian – if we are to have an economic war with Russia (and China, Iran, India and a growing part of the non-western world) then we need to move to a war economy in which nobody is left behind. Instead, they delivered a warmed-up and out-of-context version of the liberal-extremist policies which caused so much damage in the early 1980s (the price for which we are having to pay today). There is no grand vision. No plan to create a more self-sufficient economic base as the globalisation project crumbles to dust. What they offered looks suspiciously like one final blowout for the rich and one last round of austerity for everyone else, before the house of cards comes tumbling down and someone else’s government is left to deal with the fallout.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.