Related Articles

|

|

Since the 2008 crash, we’ve all had to get used to “shrinkflation” – where, at least until recently, manufacturers kept prices down by shrinking the content. A 150 gram bar of chocolate, for example, would become a 125 gram bar but would sell at the same price. Okay, that’s easy enough to understand when it comes to packaged food or cleaning products, but how is it possible to have shrinkflation at a petrol station? After all, we continue to buy petrol by the litre… and a litre of petrol is a litre of petrol, right?

Wrong! Petrol just isn’t what it used to be. Indeed, in Britain since September 2021, a litre of petrol has five percent less petrol in it. Long before that, allegedly for environmental reasons, Britain had been adding five percent ethanol to the mix. But in September 2021, this rose to ten percent – which is what the “E10” at the pumps means. Ethanol is a few pence cheaper than pure petrol, but any price saving there may have been, was lost in the post-pandemic price spike. This, in itself, might constitute shrinkflation. But the bigger problem is that the energy content of ethanol is about a third less than petrol. As Paul Hudson at the Telegraph explained last year:

“Concerns immediately arose about the fuel’s efficiency, with claims from the AA that fuel costs would rise by about 1.6 per cent purely as a result.

“That’s because ethanol is about a third less energy dense than pure petrol. In the USA, research by the Environmental Protection Agency (EPA) showed between a three and four per cent reduction in fuel economy using E10 compared with pure oil-based petrol.”

According to Kate Galbraith at the New York Times, the difference between petrol and E10 is around three miles per US gallon. So, not only did the price of petrol spike up after E10 was introduced in Britain, but we needed to fill up more often. Shrinkflation indeed:

It is unlikely that many motorists noticed. After all, the range lost from things like under-pressured or worn tyres is likely greater. Moreover, the stop-start nature of driving in urban areas – which is where most trips are made – will cause fluctuations in range anyway. And when it comes to older vehicles, most people would likely blame any consistent loss of range on wear and tear.

Nevertheless, the broad point stands – E10 petrol provides less exergy – the fraction of energy which is converted into useful work – than pure petrol. In this sense, a petrol car can be seen as a simple model for the way in which the economy as a whole uses energy. In short, the less energy that goes in, the less useful work that can be done.

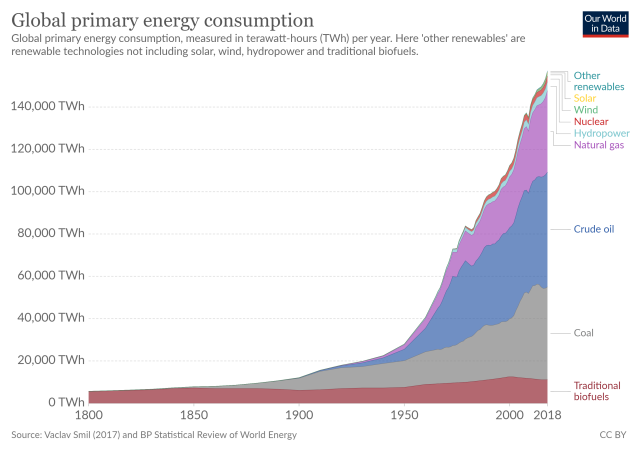

This is important because it reminds us that economics is ultimately about thermodynamics. That is, in order to produce anything requires that we must first consume energy… even if this just means eating something so that we can engage in manual labour. Today’s complex global economy depends upon millions of years of fossilised sunlight – together with a sprinkling of stardust – to provide us with the energy with which to transform raw materials into the trillions of goods and services which make the world go around. Indeed, it is now so vast and complex, that most people have lost sight of the energy which makes it all work:

For the best part of three centuries, humans have been able to add ever more energy to the mix in order to continue to grow the economy and, indeed, the human population, to undreamed of heights. So, it would be something of a problem if, say, the fossil fuels – coal, gas, and oil – which still account for some 80 percent of the energy we use, turned out to be a finite resource. This, after all, is the central problem raised by the supposedly discredited “peak oil theory.”

Not that it was ever a theory. Rather, petroleum geologists like Marion King Hubbert simply observed that there was only so much oil in the Earth’s crust, and that sooner or later, we would reach the point when we were producing the most we could ever produce. And since there was roughly a 40-year span from the discovery of an oil field to the peak of production, Hubbert was able to correctly estimate the peak of US conventional oil production. Moreover, using that 40-year timeframe, Hubbert figured that since peak global oil discovery occurred in 1964, then global peak oil ought to occur in 2004.

Okay, Hubbert was a year out on that one. The world peak of conventional oil production came in 2005, and proved to be the spark which set off the 2008 crash. What Hubbert hadn’t anticipated was the extent to which unconventional oil extraction – such as from deep sea, tar sands and shale deposits – might drive oil production up to new highs. Indeed, even recent discussion of whether a peak was reached in November 2018, might yet prove to have been premature. As Art Berman has shown, following lockdown, at 100 million barrels per day, world oil production is almost back to its 2018 102 million barrel high point.

So, does this mean that peak oil has once again been discredited? Not so fast. As Berman points out:

“The good news is that U.S. oil production has recovered to pre-pandemic levels. The bad news is that only 60% of it is really oil… The rest is non-petroleum and comes from natural gas, corn & refinery gain…

“Total world liquids production has recovered to 99% of 2018 average level but crude oil plus condensate has not and remains more than 4 mmb/d below late 2018 levels…”

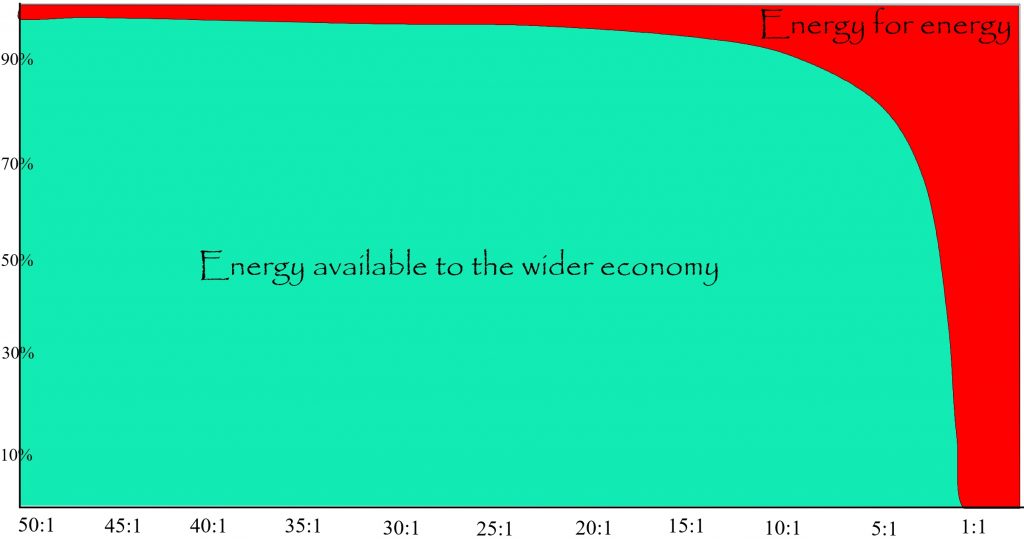

As Berman reminds us, those raising concerns about peak oil tended to get wrapped up in predictions about when it would happen. But that was never really the issue. The more important concern was the impact on a largely oil-powered economy once we were forced to get by on less oil every year. This, in turn, was always about thermodynamics rather than volumes. That is, like the E10 fuel powering your car, it is the thermal content, not the quantity, which matters. And just as your car can’t take you as far as it used to, so the economy as a whole has been unable to continue doing the things it used to prior to the November 2018 peak. As the amount of energy returned from the energy invested declines, so the wider economy must shrink:

This, of course, has been hidden to a large extent by two years of lockdown and the USA sanctioning Europe in response to Russia’s invasion of Ukraine – both of which (although they insist on misspelling them “the pandemic” and “Putin”) continued to be blamed for the economic depression by the political class. Nevertheless, the implication of the loss of thermal content in the fuels we depend upon is that even if the pandemic and invasion hadn’t happened, the process of decline would have happened anyway… just a little slower than it has done.

There is little agreement as to exactly how this will play out in practice. Conventional – i.e., wrong – economics holds that as demand for energy outstrips supply, so prices will spike even higher than they did either side of the 2008 crash. This sounds straightforward enough. Just as you have to put more E10 fuel than petrol in your car, so global industrial processes have to consume more of these lighter oil products in order to obtain the thermal content they require. The result is that, even if total “oil” production increases, its thermal content is still too low to meet global demand. Hence, supply and demand kicks in and prices rise accordingly.

Except that this isn’t what happens in the real world. As Gail Tverberg has demonstrated, what actually happens is that the weakest businesses and households are bankrupted by the higher prices, thereby generating a recession which causes prices to fall. This would suggest a period of see-sawing where every time the economy begins to grow, excess demand for oil causes prices to spike, ultimately causing the next recession. But, as Tverberg argues, it is far worse than this, because the recessionary response to higher prices deters potential investors, thereby guaranteeing future shortages as old wells deplete and new wells fail to be drilled. There is no longer a goldilocks price which is low enough for consumers but high enough for potential producers:

This suggests that the old adage that “the answer to high prices is high prices,” is not enough. Certainly, what we have witnessed over the past 18 months demonstrates the validity of the demand side of the adage – spiking fuel (and food and electricity) prices resulted in a big shift in spending away from discretionary items. In the UK, Christmas 2022 is shaping up to be the worse for retailers since the early 1980s. A similar crash in demand has also occurred in the USA, where tech firms like Microsoft and Amazon have recently announced tens of thousands of layoffs, and where a repeat of the events leading to the 2008 crash look likely.

The problem is that the supply side is not behaving in the way conventional economics expects. What ought to happen is that higher prices lead to more investment which, in turn, results in more supply. The additional supply eventually outstrips demand, and an equilibrium is achieved. But whereas a decade ago, investors were prepared to squander money in the US shale plays, this time around, investment has been muted. In part, because too many investors got burned spending billions of dollars to produce millions of dollars of fracked oil. In part, because various “green” laws and ESG regulations have turned long-term investment into a fool’s game. As Juliet Samuel at the Telegraph argues of the current European energy crisis:

“The meeting goes like this: ‘We need you!’ say the politicians. The producers scratch their heads as they mull $20 billion, 20-year investments, and wonder whether, when the war is over and the green bandwagon rolls back into town, the politicians will still sound so sweet on them. ‘Your green targets still say we need to shut down by 2030,’ they point out. To which Europe says: ‘Well, of course. Fossil fuels are evil!’”

The UK government has already responded to energy shortages by giving further subsidies to the North Sea drillers in the vain hope that a few million more barrels can be squeezed out of the depleted fields. And ultimately, other governments will follow suit because that is the only way of halting the unfolding depression – although most likely only after a few more years of failing to provide the energy needed using non-renewable renewable energy-harvesting technologies, and just making the economic crash even worse.

This though, is where the crisis before us becomes a predicament rather than a problem. Because, in a discussion with Nate Hagens on the Great Simplification channel, Art Berman drops an even bigger bombshell – the thermal content of the remaining reserves is also falling. That is, while we have long known that we have produced oil on a “low hanging fruit” basis – starting with deposits just beneath the land surface before working our way to deep sea and fracked deposits – few had appreciated the quality of the oil involved. Nevertheless, the process by which oil was created, using the pressure and higher temperature in the Earth’s crust, means that the heaviest – and thus most energy-dense – oil is found closer to the surface. And the problem is that not only have we found most, if not all, of those deposits, but almost all of them are already in decline. Deeper and smaller deposits – which account for most of what is left – have been over-cooked and over-compressed, making the oil recovered far lighter and less energy-dense. So that, even if governments act as investors of last resort in an attempt to increase oil production, the thermal content will continue to fall anyway… a bit like going from E10 to E20 and pretending that you will still be able to drive the car the same distance.

The Great Depression of the 1930s was largely caused by the declining energy return from coal, which was still the primary power-source of the European and Japanese economies. It was oil – used to power the Allied war machine during the Second World War – which put the USA on the road to recovery. And it was the switch from coal to oil power across Europe, Japan and South Korea which fuelled the post-war economic boom. This time around, there is no energy-dense alternative to oil with which to power the future economy. And whichever way you cut it, that means that we are going to be consuming a lot less stuff than before… so get used to it.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.