Related Articles

In 1927, the market price of coal spiked. As is the way with events like this, a scapegoat was easily found. Welsh coal miners had been on strike for most of the previous year, helping to create a global shortage. There was though, a deeper and potentially existential cause – the peak of coal-based coal production.

Although oil was rapidly replacing coal as the primary energy source in the USA, the rest of the world’s economies were as dependent upon coal as they had been half-a-century before. And even America was reliant enough on coal for the price spike to translate into an economic slowdown… which was a serious problem in an economy which had been experiencing the debt-based “roaring twenties,” during which almost everyone came to believe that the economy could only grow, and that tomorrow was bound to be better than today.

Economic historians remind us in lurid detail what happened next. As the economy slowed, the value of assets fell short of expectations. Millions of people who had borrowed to invest suddenly found themselves with assets which were worth less than the debt they needed to repay. For a while they stuck it out, hoping that growth would return, and values would be restored. Until, in October 1929, the big players began to cut their losses. The Wall Street Crash turned paper millionaires into paupers overnight and paved the way for the Great Depression which saw millions of Americans – and later, millions around the world – reduced to penury.

The road out of depression was far worse, involving global industrial warfare which decimated cities and economies, leaving more than 80 million corpses in its wake… but the US arms industry had a good war. And sadly, among the wealthy and the powerful, the erroneous conclusion that “war is good” was easily drawn.

Behind the awakening of the sleeping giant that was the industrial USA, though, lay oil. Without the oil to power the tanks and aeroplanes and ships and trucks, the allies could not have prevailed. Indeed, it is a measure of the power of oil that the USA was able to simultaneously fight four campaigns – Central Pacific, Southwest Pacific, North Africa-Italy, and Northwest Europe – against three enemies – Japan, Italy, and Germany – while having sufficient excess industrial capacity to provide essential supplies to its allies – Britain, the Soviet Union, and later France.

Insofar as there was a post-war boom, it was the result of the old, coal-powered economies of Europe, Japan and South Korea using US dollars to fund the transition to oil – a process that is still within living memory. In the two decades 1953 to 1973, the world witnessed more economic growth and trade than had occurred in the previous 150 years of the coal age – creating a modern world which increasing numbers of us realise is already past its peak.

So, here’s a thought experiment – what would have happened in the 1930s if there was no such thing as oil?

First, although the least understood, is that productivity would have slumped across the industrialised economies as the coal which powered the machinery became harder and more expensive to obtain. Gradually, processes which had been automated would become labour intensive again. International, and even inter-regional trade and transportation would become harder to maintain, forcing a re-localisation of the economy. And ultimately, this economic slowdown would result in everybody becoming poorer (even if some became poorer than others).

Government – which more often messes things up than makes them better – would undoubtedly fail, as orthodox economic policy not only failed to restore prosperity but appeared to make things worse. This, in turn, would lead to the growth of unorthodox political ideas and the arrival of demagogic leaders who promised to make countries great again… but absent an energy source more powerful than the fast-depleting coal, even the most benign dictators would fail to deliver any kind of new deal to turn things around.

Elected politicians would also struggle to overcome the vested interests in the permanent state and the wider corporate ownership class, which would only allow for policies which did not threaten their own prosperity. The likely result would be a downward dumping which attempted to make the poorest people take the greatest hit to their prosperity. A new lower class, living in precarious conditions would likely emerge, trading labour for food and shelter rather than the monetary wages of the earlier age… a “precariat,” if you will. Ultimately though, much of the nominal wealth of the elites – government bonds, corporate shares, numbers in bank accounts, etc., – would be rendered worthless by a collapsing economy that has no pathway to sustainability, still less economic growth.

In the end, most of the corporate elite would probably be dispossessed as one or other version of collectivism rose to power in a last-ditch effort to restore the broad prosperity of the earlier age. But without the energy to make things happen, even the brutality of a Stalin, a Mussolini, or a Hitler could only preside over a further collapse and a slide back to the agrarian localism of a much earlier age.

But, of course, the oil was there… in vast quantities. And its raw power propelled the USA and its allies to victory in the war and created the conditions for the unprecedented post-war boom… the “normal” that we have been somehow failing to get back to since the 1970s.

Despite its apparently small increased power compared to coal – around 10 megajoules per kilogram – the additional power provided by oil shaped the modern world. But its high points – sending men to the Moon, commercial supersonic flight, transplant surgery, microprocessors, etc., – are half a century or so behind us. Indeed, look closely enough and you will probably notice that a good deal of the built environment from those days is falling apart.

Oil, it turns out, came with the same issues as coal. It is a finite resource (at least on any practical timescale) which has been developed on a “low-hanging fruit” basis… starting with the cheapest and easiest deposits then moving on to the difficult and expensive. And yet all the while being expected to meet the demands of a rapacious debt-based financial system for permanent economic growth. So that each additional unit of energy that has to be invested in recovering the more energy-expensive oil is a unit of energy no longer available to be converted into profit and interest repayment by the corporations and the banks.

Notice too, that the economic landscape today has a certain resonance with the coal depression of the 1930s… remembering that history rhymes rather than repeats. Doesn’t the gig economy look a lot like those lines of unemployed people desperate to find any kind of work? Aren’t the tent cities that are now commonplace (if hidden for cosmetic reasons) in almost every western city very similar to the shanty housing of the depression era? Might foodbanks be a modern iteration of the charity soup kitchens of the 1930s?

The political leaders and captains of industry of the coal age might be forgiven to some extent for their failure to understand the central position of coal to their way of life. Then, as now, a few Cassandras– like William Stanley Jevons in The Coal Question – understood that in consuming its coal at an ever-faster rate, the British Empire was ultimately bringing about its own demise. But most of the economists of the day blithely promised that as one coal deposit depleted another would be found… and, indeed, with the development of oil-powered machinery, previously unrecoverable coal was eventually produced.

In this sense though, the obvious absence of an alternative to oil should have been a cause for concern from the outset. Indeed, in the immediate post-war years it had been possible to accurately predict the peak of continental US oil production based upon a 40-year lag between the discovery of an oil field and the peak of its productivity. Since peak oil discovery in the USA was in the early-1930s, the peak of US production should have arrived around 1970-71… which it did. And since the peak of world oil discovery was in 1964, it followed that the peak of world production would be in 2004-05… which it was.

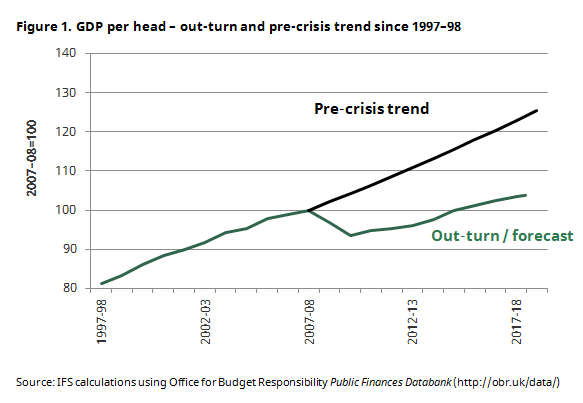

As happened in 1927 with coal, the 2005 peak in conventional oil production created the same price spike which fed through to general price rises across the economy. This time, aided by the fumbling incompetence of central bankers, rising interest rates were added to the mix. But the result was the same – a banking and finance crash followed by a depression that we have never recovered from. Indeed, the only reason that we witnessed even the anaemic growth of the 2010s was the American so-called “fracking miracle.”

It wasn’t really a miracle though. Both the discovery of the shale plays and the invention of the fracking technology had occurred decades before the 2008 crash. The reason the shale plays remained undeveloped was down to cost. With oil prices in the 30 to 50-dollar-a-barrel range there was no way fracked shale oil could turn a profit. But the oil peak of 2005, along with the post-2008 financial landscape changed that.

World oil prices exceeded $100-per-barrel either side of the crash, prompting economists to predict $200-per-barrel oil in the 2010s. Suddenly, fracking looked like a good bet for investors. And this was aided by the low-growth, low-interest environment following the crash. The return on safe investments was negative once inflation was taken into account. And even riskier dabbling in the stock and bond markets brought relatively small returns. For the investment chancer looking to make a quick fortune, junk bonds were the only game in town. And the best junk bonds on the market were the bonds offered by the fracking companies.

The fracking experiment taught us another important lesson… if only we had heeded it. $100-a-barrel oil (at 2008 values) turned out to be unsustainable. As businesses and households adjusted their spending to account for the higher oil price, discretionary sectors of the economy slumped. With less economic activity following reduced discretionary spending, demand for oil slumped… as it happened, just at the point when millions of barrels of fracked oil were arriving on the market. The oil price slumped. And with the exception of a few companies drilling in a handful of “sweet spots,” the fracking companies went bust.

Far from the establishment media’s “Saudi America,” and the “century of energy independence,” the hydraulic fracturing of the North American shale plays bought us and additional decade of oil production growth. But with no serious replacement on the table, that decade would have been best used to mitigate the inevitable economic shrinking and disintegration that is now washing over us. American, and global oil production finally peaked in November 2018. By the middle of 2019, the global economy was entering a recession – although this was overtaken by the pandemic lockdowns and restrictions, followed by the insane attempt at economic warfare with one of the most resource-rich states on the planet. So that even now, in the midst of a global energy crisis and a gathering globally-synchronised recession, establishment politicians, economists, and media seem oblivious to the energy shortages which are driving us to ruin.

Maybe it was inevitable. A species which seemingly evolved to deny death and despair was able to treat oil reserves which it knew to be finite and consume them as if they would last forever… or at least until clever people somewhere else came up with an alternative. And yet even after global peak conventional oil had sent the global economy into a death spiral, we somehow managed to pretend all would turn out well, and that the final recoverable deposits of unconventional oil would somehow be infinite.

How different might the post-war years – or even the last 16 years – have been if we had treated cheap oil as the temporary gift that we should have understood it to be?

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.

{kind=link}

{kind=link}

{kind=link}