Related Articles

For once, the UK government has managed to do the right thing… albeit for the wrong reasons. I refer, of course, to the emergency powers rushed through parliament yesterday, which de facto re-nationalise what remains of Britain’s virgin steelmaking – the mendaciously named “British Steel” plant (it is Chinese-owned) in Scunthorpe. Introducing the emergency legislation, Keir Starmer focussed on saving jobs at the plant:

“We are acting to protect the jobs of thousands of workers, and all options are on the table to secure the future of the industry.”

Reasonably and predictably, Plaid Cymru complained about the double standard involved in saving Scunthorpe despite allowing the closure of the (Indian-owned) Port Talbot blast furnaces last year. English jobs, apparently, are more important than Welsh jobs. But jobs aren’t really the issue, and the failure to grasp this points to a political class which remains entirely detached from the real world.

The reason why virgin steel is essential, is because it is a key component at the very base of any complex industrial economy. So that, while there are many applications which can use inferior steel grades and recycled steel, much of our critical infrastructure cannot (although, for now, we are able to import virgin steel at a cheaper price than we can make it at home). For example, we cannot manufacture and deploy wind turbines without virgin steel. And good luck keeping the Severn Bridge going if you intend using recycled steel in those essential suspension cables which are coming to the end of their expected life.

Saving Scunthorpe is essential… but it may not be sufficient. Indeed, like so much of the UK’s critical infrastructure, we have only avoided the complete unravelling of our economy because of the prolonged depression since 2008. As UK Steel points out:

“This latest report shows that in 2023, UK steel production and demand plummeted to new historic lows of 5.6 and 7.6 million tonnes (Mt) respectively, well below the levels seen even at the peak of the pandemic in 2020. UK production in 2022 had already marked the lowest level since the Great Depression, but in 2023 it dropped by a further 6%, while demand fell by 14% on year.

“All this while the import penetration in the UK market has continued to increase. In 2023, net imports stood at 4.6Mt claiming a 60% import share up from 55% the year prior. While overall imports fell in absolute terms by 5%, volumes increased from Asian origins, notably India and Vietnam, as well as France, all of which benefit from much lower electricity costs. Weak demand in China is also having knock-on effects on wider trade flows from Asia.”

One way in which the UK government intends increasing domestic production is through the construction of a steel recycling plant to replace the blast furnaces at Port Talbot. The UK generates 10-11 million tons of scrap steel every year. And so, on paper at least, the new arc furnace at Port Talbot (assuming we can obtain the steel to build it) will have plenty of stock for the 3 million tonnes per year of recycled steel it is expected to produce… but not so fast.

Just because something can be done in theory is no guarantee that it will happen in practice. And this may prove particularly true for UK steel recycling. As Dr. Russell Hall, Dr. Wanrong Zhang, and Dr. Zushu Li at Warwick University explain:

“To increase the electric arc furnace steel production capacity in the UK would require significant investment, estimated costs for an electric arc furnace steel manufacturing site could be over £1bn depending on the scale, location and complexity of any downstream steel production required. Electric arc furnace technology would need to be imported into the UK as there are no UK based manufacturers.

“There are a number of potential barriers to enabling increased recycling of scrap steel in the UK which need to be overcome. The business alignment between steel manufacturers and scrap suppliers (merchants) needs to be improved to enable a more efficient industry. The standards used to sort scrap steel in the UK are not sufficient to ensure that the scrap steel received by steel manufacturers is of the quality and consistency required to be easily recycled into high quality steel grades. The technology currently used to assess and sort the different grades and chemistries of scrap steel is not advanced enough, often scrap quality monitoring is completed by visual inspection, leading to poor quality scrap steel being used in the steelmaking process. The transition from the blast furnace ironmaking – basic oxygen steelmaking process to electric arc steelmaking is not straight forward, and there are a number of challenges in knowledge/expertise, energy supply and logistic that the steel manufacturers need to face in order to make the transition, in addition to meeting the customer requirements (e.g. steel grades, quality and price).

“If there is to be significant investment in the UK for electric arc steelmaking then any factors that impede investment will need to be overcome. Barriers to investment are mostly fiscal, with some affected by geography. UK steel producers have an operating cost disadvantage when compared with many other steel producing countries for electricity costs, and the cost of electricity becomes more important with the electric arc steel manufacturing process as electricity provides the bulk of the process energy. A similar overhead cost disadvantage is seen for the UK steelmakers for business rates. Business rates in the UK are charged on the rateable value of the company, which includes physical assets. Steelmaking equipment is very expensive and investment into new plant increases business rates even if it serves to increase efficiency or decrease emissions. Greenhouse gas emissions for UK steelmakers are taxed under the UK emissions trading scheme (ETS), which caps the industry’s emissions. The UK ETS is roughly in-line with the EU ETS and has been designed to give a seamless changeover in emissions taxes post Brexit. Emissions tax regimes are an investment burden when compared against steelmaking countries where there are no carbon taxes. Finally, significant investment barriers can be associated with geographical physical and economic factors such as land prices, power generation facilities, remediation costs for closing current plant, infrastructure and labour sources.”

One is reminded here of the anecdote about asking for directions in Ireland, to which the answer is, “well, you don’t want to start from here…” Or, to state the problem more seriously, we are now reaping the consequences of decisions made half a century ago, when the neoliberals made the claim that we no longer needed domestic critical infrastructure because Free Trade™ would allow us to import anything we needed.

The interconnected predicament that this has created can be seen in the similar mismatch with electricity imports. For several decades, UK governments of all colours have blithely allowed domestic electricity generators to close in the belief that we will be able to source all the electricity we need from abroad (incidentally, I wonder whether a large part of the political class is sufficiently IQ-deficient to imagine we can load it onto ships and store it in warehouses). But this assumes that while we run an electricity deficit of around 20 percent, neighbouring countries will run a large enough surplus to supply us without noticeably raising prices. Except, predictably, that didn’t happen. France and Belgium managed to hold up their own generation by sticking with nuclear (making France the least carbon-intensive generator in Europe) but Germany chose to scrap its nuclear and coal plants in the insane belief that its economy could run on intermittent wind and solar backed up by cheap Russian gas (which ended with sanctions and the US sabotage of the Nord stream pipeline). Norway – which has a tiny population but lots of hydroelectric generation – has in recent years, had to act as Europe’s emergency supplier. Although the pan-European shortages have caused eye-watering electricity prices as European electricity suppliers bid the price up in an attempt to plug the gap in their own generation… something the Norwegians may bring to an end because they resent paying for it. Less obviously, a large part of Europe’s heavy industry and agriculture has been forced to close due to the high price of electricity – a particular issue in the UK, which now has the highest industrial electricity price in the world.

The result, when it comes to steel making, is that while recycling may be (a little) “greener,” it is excessively expensive compared to producing steel in a coal-powered blast furnace (which, in Port Talbot’s case, used to recycle steel too)… which brings us to the core issue which the political class seems determined to ignore – that this has only become an issue today, because the Trump administration kicked the proverbial board up in the air, and nobody is sure where the pieces are going to land.

That is, for eight decades the “collective west” – North America, Europe, Japan, South Korea, Australia and New Zealand – has lived comfortably beneath the USA’s economic and military umbrella. And following the collapse of the Soviet Union in 1991, the western political class assumed that they could dictate the economic rules to the whole world – engaging in colour revolutions and military invasions where necessary. Among those rules was a version of Free Trade™ which amounted to modern imperialism through which access to the US dollar and its associated currencies was only granted in exchange for preferential trade terms. Poor countries in the “global south” – Asia, Africa and South America – provided cheap goods and resources in order to access the dollars needed to run their countries. In Europe, this “rules-based international order” came with the added benefits of the closed trading bloc of the European Union, access to which required further sacrifices on the part of those poor countries in the global south.

This speaks to an important form of denial which is now coming into focus – and which runs much deeper than the stubborn refusal to consider the reasons why the Trump administration is currently tearing up the established rules. This is summarised by Charles Leon in “Will the Sun rise tomorrow?”

“Inductive reasoning has allowed us to build nuclear power stations, put a man on the moon, discover the human genome, and develop supercomputers. So, it seems that induction and assumptions are, after all, a reliable way to produce true beliefs. You might say that induction has worked up to now and therefore will continue to work in the future. We’re back to the same circular argument.

“If we didn’t believe in our inductive thinking other people would think we were insane. Induction supports insane ideas and concepts about the future as much as ideas that (seem to be) sane and rational.”

Without the in-built assumption that tomorrow will be pretty much the same as today, we couldn’t function. We would, instead, have to start each day in a child-like state in which everything is new and unfamiliar, and in which we must re-learn everything. But we have evolved to ignore the fact that almost everything in our lives is in a constant state of flux. Okay, some of that flux – like the slow speed at which the Sun is changing, or the gradual movement of the moon away from the Earth (about the same rate as North America is moving away from Europe) – is so gradual that we need not concern ourselves with it. We can be certain the Sun will rise tomorrow, but we should be far less certain when considering if, for example, the banks will still be open on Monday, or if the electricity supply can be guaranteed next winter.

Among the biggest failure of neoliberal governance, even after the shocks of 2008, 2020, and 2022, is the tendency to assume that tomorrow will be the same as today. So that, in the western economies at least, we have assumed, for example, that borrowing trillions of dollars, euros, and pounds into existence to prevent the rebalancing of the financial and real economies that those crises would otherwise have resulted in, came at no cost. Whereas, in reality, western governments are currently rolling over much of that debt at unaffordable rates of interest, and at a time when investors are reluctant to buy more government debt.

The UK response to this growing crisis has been to turn to the standard neoliberal playbook… which is why there is no discernible difference between the current Labour (in name only) government and the Tories they replaced. Interest rates must be kept high to secure foreign investment, even though this is crippling UK businesses. At the same time, taxes have to rise to reassure those same foreign investors that the UK will be able to pay the interest on its debt. And then, because of the gap between borrowing and spending, further austerity cuts have to be imposed… with the government choosing to hit the most vulnerable the hardest.

The people behind Trump, in contrast, have concluded that the gathering storm cannot be addressed within the pre-existing neoliberal framework. Debt ceilings have failed time and again, as politicians of all shades have given way to public pressure rather than face the likely economic fallout from closing down swathes of the unelected bureaucracy. Austerity cuts, meanwhile, only serve to deepen the growing “crisis of under-consumption” which threatens to destroy swathes of western retail and service businesses. Worse still, as the crisis deepens, the majority of the world’s countries are looking favourably to the BRICS bloc as a potential alternative to the “exorbitant privilege” of the US dollar.

What Trump’s people appear to be attempting is to devalue the outstanding debt without losing the US dollar’s reserve currency status. But this cannot be achieved with a trade deficit this big, since an uncontrolled devaluation – which is the only alternative on the table – would result in hyperinflation as the price of imported goods – many of them essential to critical infrastructure and military needs – had to be paid for with devalued currencies.

Trump has had to row back some of the tariffs, simply because despite the huge potential for self-sufficiency in North America, the US economy is currently deeply dependent upon imported resources and goods. And while some of these may be substituted in the medium-term, for now, the USA has no choice other than to import them.

The problem for the UK, and for Europe in general, is that it lacks even the material advantages still held by the USA. The UK’s oil and gas reserves were plundered in the 1980s and 1990s in pursuit of a rentier economy based on the City of London which produced very little productive investment in the wider economy. Critical resources like coal mining, gas drilling, steel making, electricity generation, food production, and oil refining, were offshored in the belief that an over-valued pound would always be available to allow us to import whatever we needed when we needed it… and that this would be as true tomorrow as it was yesterday.

In this respect, the Trump administration may have done the UK and Europe a favour by exposing our structural weakness. But it is far from clear that the current political class fully comprehends its predicament. Notably, even after assuming control over British Steel, Business Secretary Jonathan Reynolds has said that:

“The emergency legislation was a ‘proportionate and necessary step’, adding he wanted it to be a ‘temporary position’ with the powers not lasting ‘any minute longer than is necessary.’”

The underlying assumption being that tomorrow will revert to being like yesterday, with Trump’s tearing up of the global rules – and more importantly, the emergence of a multipolar world order of a kind not seen since the 1930s – is merely temporary, and that the UK will soon return to running on foreign debt and cheap imports. And perhaps this form of denial is the only thing the current UK government can find – temporary – salvation in. Because, in the new, multipolar trading relations which are emerging – themselves largely a product of global energy and resource depletion – the economic task facing a spent economy like the UK’s is daunting.

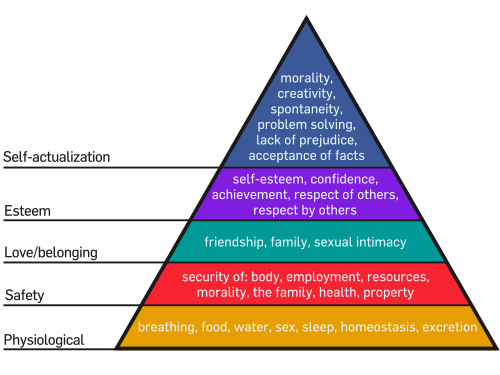

An economy has a hierarchy of needs similar to Maslow’s hierarchy for individual humans. Sufficient food, clean water, clothing and shelter to keep the population alive is at the very base – with most revolutions beginning with rumbling bellies rather than intellectual ideologies. But even to deliver these requires critical infrastructure which includes steelmaking, water and sewage treatment, electricity generation, oil refining, and transportation – all of which have, in the UK, been undermined in the pursuit of private profit. And while we can visualise these as independent systems, in practice they are highly interdependent. You can’t make steel without water, coal and electricity. And even if you could, without transport, you couldn’t use it. But without the steel, you can’t have the rail or road systems or, indeed, the new electricity generation to power the steelworks. Without oil refining, you cannot run the diesel trains and trucks that are the backbone of the transport system. And without the trains and trucks – along with diesel powered machinery – you cannot build anything.

All of this basic – and critical – infrastructure must be in place before we can enjoy the much broader discretionary consumption/landfill economy that we have taken for granted for decades. And that is a major problem for countries like the UK which have spent much of the last 50 years outsourcing their critical infrastructure to states that have lower wages and fewer regulations. Because one way or another, the cost of imports is rising and we don’t have much in the way of domestic manufacturing to pay for them (which, by the way, is why the UK was on the lowest tier of Trump’s tariffs).

Instinctively, many among the UK’s political class see rejoining the EU as the obvious solution. But again, this is seeing the EU as the relatively prosperous trading block that it was prior to 2008 – or at least prior to 2022. That EU, however, has disappeared in the swathe of de-industrialisation which followed the ill-conceived sanctioning of cheap Russian oil and gas (along with coal from Kazakhstan, which is one of the problems currently facing British Steel). The EU – like the UK – has been responding to the unsustainable rise in energy costs by holding down wages, cutting spending, increasing taxes, and most recently by attempting to borrow their way out of debt. The result is that discretionary spending has collapsed across those EU states where Britain had previously sold its exports… indeed, contemporary Europe, both economically and politically, looks a lot like the Soviet bloc in the late 1980s.

It is not enough then, for the UK government to “temporarily” take control of its remaining steelworks. Indeed, even if it had also saved Port Talbot last year, it would still have faced a massive deficit in the very likely event that it needs to reshore much of its critical infrastructure. What is required is a root and branch rebuilding of the UK’s critical infrastructure – within which I include the reshoring of as much food production as possible. This, in turn, requires us to bin the neoliberal order as no longer fit for purpose, and to return to a mixed economy – with critical infrastructure in some form of public ownership or administration – so that an inevitably smaller economy begins to work for the people rather than the other way around… far from being the same as yesterday, that is, we need our future to be very different.

As you made it to the end…

you might consider supporting The Consciousness of Sheep. There are seven ways in which you could help me continue my work. First – and easiest by far – please share and like this article on social media. Second follow my page on Facebook. Third follow my channel on YouTube. Fourth, sign up for my monthly e-mail digest to ensure you do not miss my posts, and to stay up to date with news about Energy, Environment and Economy more broadly. Fifth, if you enjoy reading my work and feel able, please leave a tip. Sixth, buy one or more of my publications. Seventh, support me on Patreon.

{kind=link}