Related Articles

Oil and Gas UK – the industry trade body – has its annual report out today. The report seeks to put a gloss on the future of an industry whose stay of execution is only temporary. According to Oil and Gas UK:

“Almost $6 billion worth of mergers and acquisitions have taken place in the UK oil and gas sector in the first half of the year – sending a strong vote of confidence in a basin that has been grappling with the challenges of a major downturn…

“Although market conditions remain difficult, the report demonstrates that the UK sector is reinventing itself. It is differentiating its offering from competing oil and gas provinces with its efficiency gains, fiscal competitiveness and world-class supply chain. While investors still want more certainty over Brexit and clarity over the role of oil and gas through a more comprehensive energy policy, the transformation underway is restoring the UK’s position as an attractive basin for investment – and one still supporting over 300,000 UK jobs.

“The challenge now is to ensure this renewed interest in the basin translates into tangible activity that could help unlock around £40 billion worth of potential development opportunities known to be in company business plans.”

The Oil and Gas UK report was afforded some background cheering from the Telegraph, which announced yesterday that:

“A boom in new projects has already unlocked an extra 140,000 barrels of oil and gas a day so far this year, and analysis from oil specialists at Wood Mackenzie suggests the 2017 total will reach 230,000 new barrels of oil and gas a day.”

Even the Telegraph is obliged to acknowledge that most of these ‘new’ projects are actually the result of investment in exploration and recovery made at the beginning of the decade when oil prices were above $100 per barrel. Meanwhile, even the conservative and usually uncritically pro-business BBC conceded that:

“The number of job losses in the UK oil and gas sector was worse than expected last year… The oil and gas industry still supports more than 300,000 jobs across the UK but that is 150,000 less than the peak in 2014.”

The BBC also report that almost all (£5.8bn) of the £6bn worth of mergers and acquisitions claimed by Oil and Gas UK comes from Total’s buyout of Maersk’s North Sea assets.

In the end, even Oil and Gas UK has to admit that all is not well for a British energy industry that is increasingly dependent upon subsidies and tax breaks to stay in business. Deirdre Michie, Chief Executive of Oil & Gas UK explains that:

“There are still serious issues facing our industry which has suffered heavy job losses since the oil price slump. But we are hopeful that the tide is turning and expect employment levels to stabilise if activity picks up…

“While industry will maintain its relentless focus on improving its cost and efficiency performance, Government can continue to play its part – by developing a clear energy policy that reinforces the role for oil and gas in the Industrial Strategy, supporting a Sector Deal and confirming in the Autumn Budget that decommissioning tax relief will be modified to support further investment activity.”

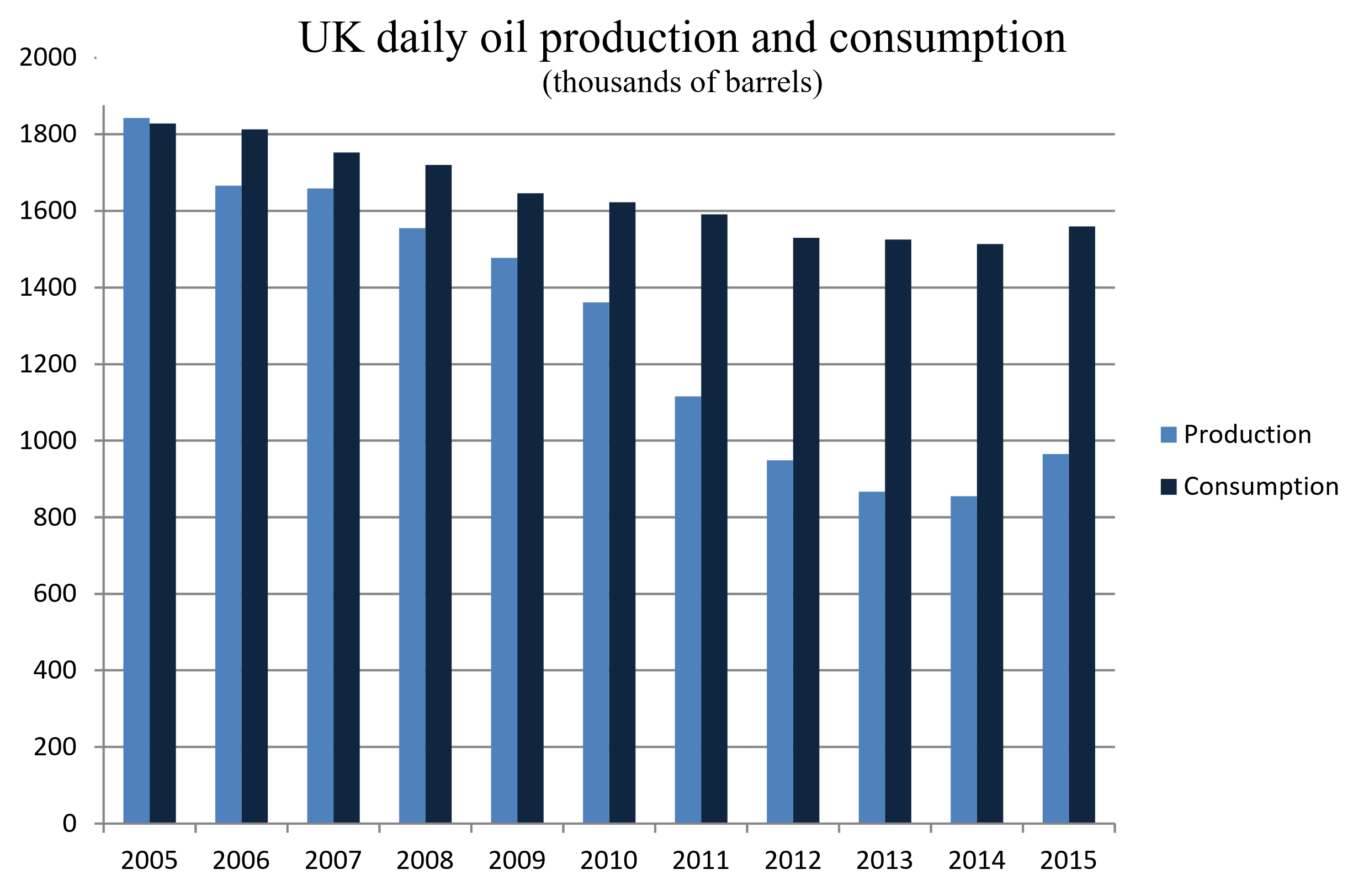

According to the BP Statistical Review of World Energy 2016, the UK has 2.8bn barrels of proved reserves (the amount of oil that can be profitably recovered; based on what the companies are legally obliged to report to the authorities rather than what they write in their investment brochures). For what it is worth, at today’s rates of production, that is somewhere between 7.5 and 8 years’ worth. In the event of oil prices rising above $100 again, this amount will rise. But bear in mind that with prices above $100 per barrel, the cost of recovering oil will also rise significantly.

Nor does an additional 230,000 barrels of production (which may just mean extracting the reserves faster) help matters significantly. Even if UK production rose by that amount, this would only bring production back to 2011 levels of output – still around 50 percent less than peak production in 1999. Nor will it do much to halt the UK’s growing dependency on oil imports:

A more realistic view of the North Sea was provided in a report for investors by Crystol Energy last year:

“The North Sea is a mature oil and gas province. Output from the two main producers – Norway and the United Kingdom – has peaked and the remaining reserves to be exploited are smaller and/or more technically challenging than those developed in the past, thereby shrinking potential returns. As several fields approach the end of their commercial lives, the decommissioning of offshore platforms and the accompanying bills are looming on a scale not seen before anywhere in the world.”

UK Oil and Gas are notably reticent about the decommissioning costs alluded to here. The exact costs are unknown. However, the cost could rise to £60bn to remove around 470 platforms, 5,000 wells, 10,000km of pipelines and 40,000 concrete blocks from the North Sea. That’s a little over 1.5bn barrels worth of oil at today’s prices. So, in effect, 1.5bn of the 2.8bn remaining proven reserve will have to be sold just to cover the cost of decommissioning, leaving just 1.3bn barrels (a little above £50bn at today’s prices) to cover operations, return investment to shareholders and pay taxes.

It doesn’t take a genius to work out that the energy industry will not be paying for decommissioning. Instead, as is the wont of private corporations, they will continue drilling for as long as there is an income to be made before filing for bankruptcy and leaving taxpayers to clean up the mess. The real question is how much longer they can persuade investors and politicians to keep throwing funds at an industry whose demise is already visible.

There is a British saying that, “you can polish a turd, but when you’ve finished it is still a turd.” Maybe it is time the UK oil and gas industry stopped polishing.